Taiwan – what voters should ask about the economy

This note is a bit different to our usual offering. It is still relevant to investors, but it is more of a guide to the economic issues that I would be thinking about if I were a voter in Taiwan. That includes one observation, and five questions that politicians should be answering.

I am not a voter in Taiwan, but it is where I live, mainly in Taipei, with frequent visits to a village in the countryside of the south country of Yunlin. Taiwan is also where I've spent most time on a never-ending mission to master Chinese, with more than two years in full-time, overly intensive language school – in 2000-01, and more recently 2021.

My life in Taiwan is probably easier than that of many of the people who actually are voters. I work at home, which doesn't mean I don't complain about wages – if you don't yet subscribe to EAE but have an interest, please (!) let me know – but I'm not living in a cramped flat and doing the shift work in 7-11 that has become stereotypical of the daily grind of life in urban Taiwan.

I have no familiarity with the stresses of raising kids. To be clear about my biases, if I was still working at the EIU, I'd probably give Taiwan a '5' rating for infrastructure, simply because of the three 50m swimming pools within a 15-minute walk from our flat. However, being of a certain age, we do continue to experience the worries of trying to care for elderly parents. I'm not sure if that is any more difficult in Taiwan than in the UK, though the challenges aren't quite the same.

My first experience with politics here was when I was working at the EIU, arranging to meet Chen Shui-bian on a visit to London before he became president in 2000. His translator at the time was Hsiao Bi-khim, the DPP's current vice-presidential candidate. Before either got the top job, I was also fortunate enough to interview both the current DPP president Tsai Ing-wen, and her KMT predecessor, Ma Ying-jeou.

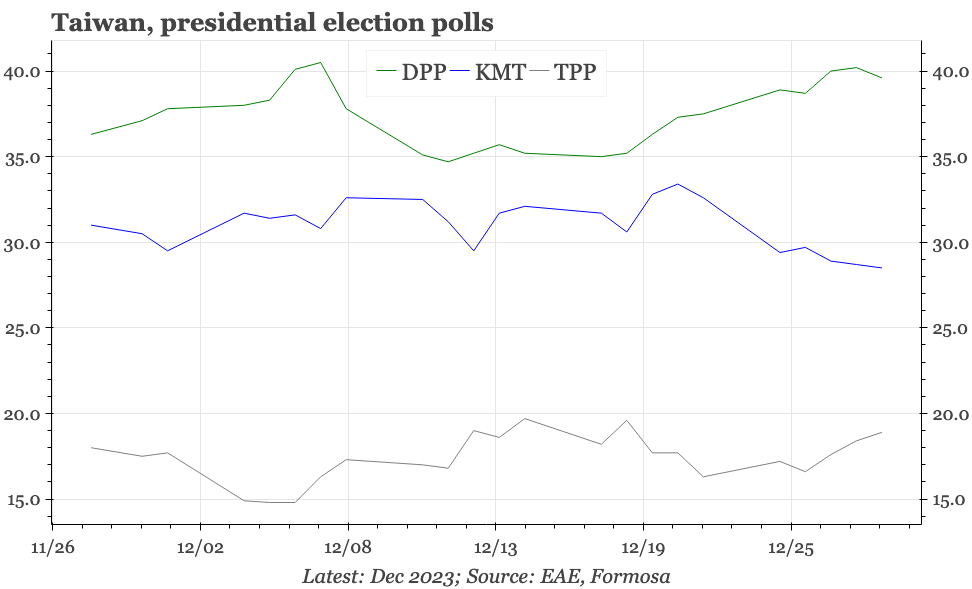

This isn't to imply that I am either a great networker, or an expert on politics in Taiwan. Reflecting Taiwan's diplomatic isolation, it is relatively easy to get access to politicians and officials here (in this respect, China couldn't be more different). As for politics, in Taiwan or elsewhere, that isn't my focus – if you want to know about it, there are much better places to look than here. That said, even for the experts, I don't think anyone has really strong conviction about who will win the presidential election on the 13th January. Lai Ching-te, the candidate of the governing party, the DPP, is the front-runner, but his lead isn't unassailable.

Anyway, the point of all this background is just that I have some familiarity with on-the-ground developments here. That I think is worth knowing, when my usual perspective is poring over economic statistics to try to work out where the macroeconomy is heading in the context of global developments. This top-down, comparative approach isn't one that is shared by the average voter. In terms of the economic statistics, that shouldn't be a surprise, being true in most democracies. It would be perhaps less expected, given Taiwan is the very definition of a small, open economy – exports account for 65% of GDP, much more even than Korea's 40% – that there also isn't much appreciation of the global environment in which Taiwan exists. But I am struck by the lack of global perspective in much of the domestic discussion about the issues facing Taiwan.

With all that in mind, this note isn't directly focused on markets and macro. It should still be relevant to anyone interested in those issues, but instead the focus is voters in Taiwan, presenting a guide to the economic issues that I would be thinking about if I was a voter as well. These start with an observation, which is followed by five questions that I would be asking politicians. Inevitably, one of those is why the TWD is so cheap.

Taiwan's economy has been very successful, under either party

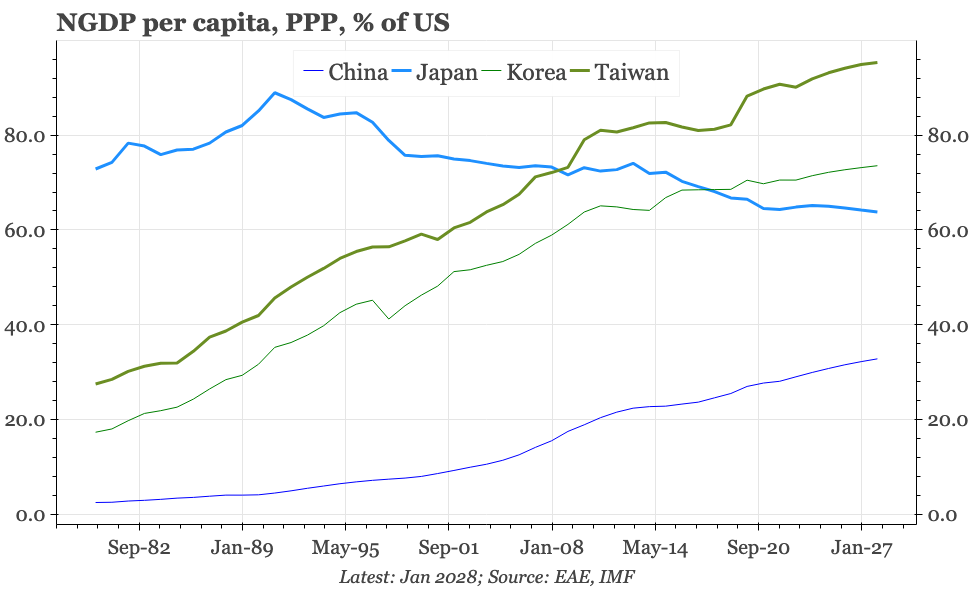

History suggests it doesn't really matter which party wins: in the very broad sense of the average standard of living, the direction is up. Taiwan's PPP GDP per capita has now reached 90% of US levels. This is impressive, making Taiwan one of the few economies to have avoided the middle income trap and become a rich economy. This is an achievement that voters of all persuasion should be more aware of, and prouder about, than they usually are.

That this isn't better appreciated is partly because of Taiwan's odd international position; not being in the UN, Taiwan also isn't a member of the OECD, and so doesn't show up in most easy global comparisons. Of course, it is also true that PPP GDP isn't a perfect measure of living standards. It doesn't capture inequality, or the high cost of housing that is a key complaint of young people in Taiwan. Equally, though, nor does it include other aspects that improve the standard of living. As an example, Taiwan features highly in most rankings of the best health systems in the world.

Why isn't the exchange rate stronger?

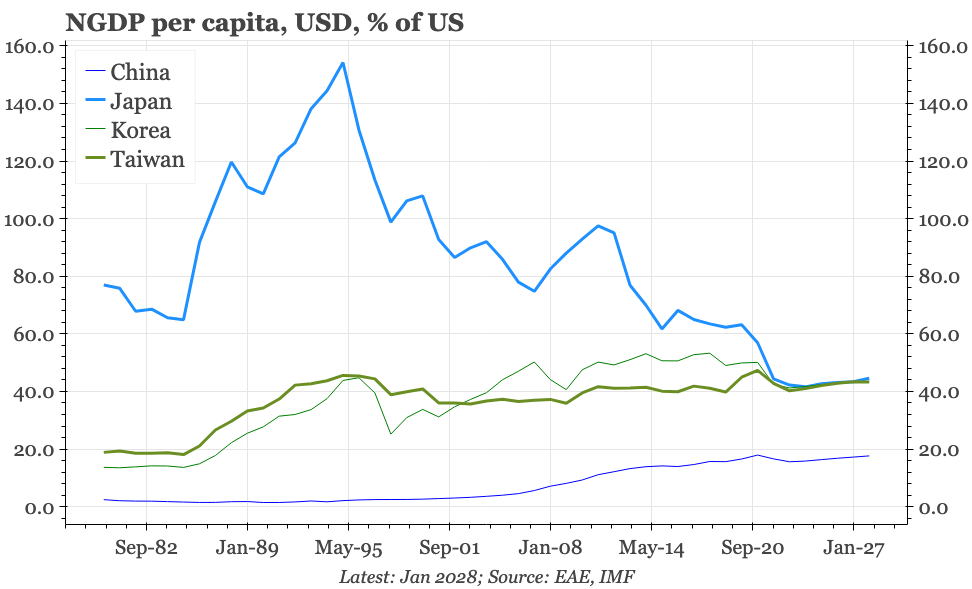

Judged in USD rather than PPP terms, and the record of economic development looks nowhere near as strong. The gap between these two measures shows, of course, that the exchange rate hasn't been appreciating. The structural weakness of the TWD is as remarkable as the rise in PPP standards of living is impressive. This isn't how economic development, in general, should work. And it looks particularly odd in Taiwan's specific circumstances, namely the importance of exports, and the incredibly high external surpluses. The current account surplus has been over 10% of GDP every quarter since 2013. As a proportion of GDP, and even in USD terms, Taiwan's stock of net foreign assets is the fifth largest in the world.

This lack of currency appreciation matters for ordinary people, affecting their purchasing power. This is clearest when Taiwanese want to travel overseas, or when they calculate the USD value of their TWD incomes and compare that with the earnings of friends and relatives working abroad. The weakness of the currency is therefore one important – and too often under-appreciated – component of perhaps the most common complaint heard in Taiwan: that wages are too low. Investors are naturally interested in trends in the TWD. But votes should be too, asking their politicians why the currency isn't much stronger.

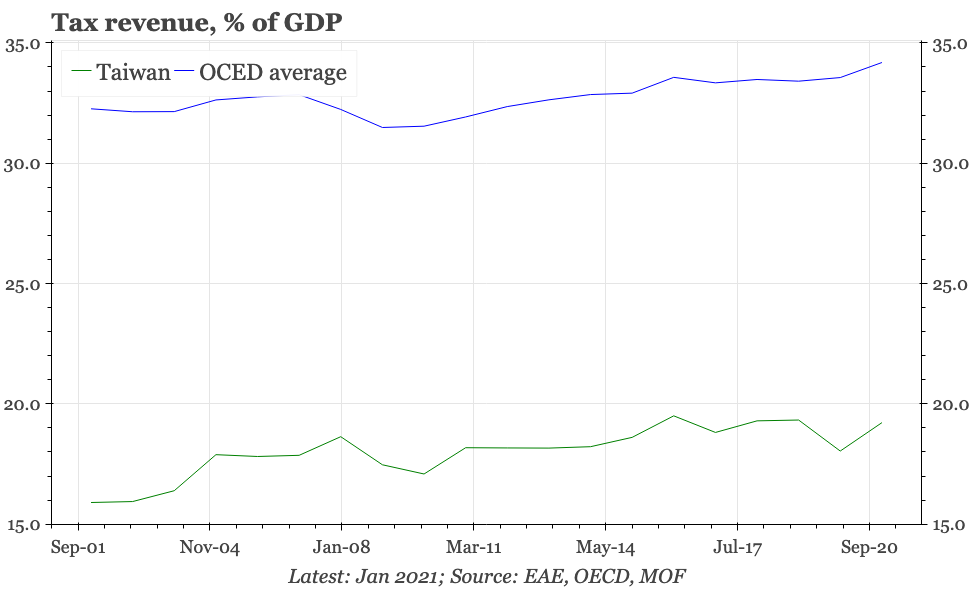

Why isn't the state bigger?

Low wage growth is an issue in Taiwan, but when thinking about disposable incomes, it is also worth remembering that the tax burden in Taiwan is also amazingly low. Overall government revenues are less than 20% of GDP, substantially below the OECD average of almost 35%. Tax on personal incomes is only 3% of GDP. To be frank, Taiwan looks so different on these metrics that I worry that there's something wrong with the data, but government finances is one of the rare sectors where Taiwan is included in the IMF's global datasets. It fits with the anecdotal picture, where a lot of people work in the large semiformal sector of family businesses. A friend who works in the formal sector said his wife complains that he's the only person in Taiwan who pays any income tax.

This low tax take doesn't mean the government needs to borrow a lot. Even before covid, public debt was below average levels in the developed world; with Taiwan avoiding the lockdowns experienced in many other countries, the gap has grown only bigger since 2020. The flipside of the low tax take is thus equally low government expenditure. This is striking, given Taiwan would seem to be needing to spend lots on defence. It is also important for the pocketbook issues that voters care about: if welfare is suffering because of low wages, then there's plenty of room for fiscal policy to help.

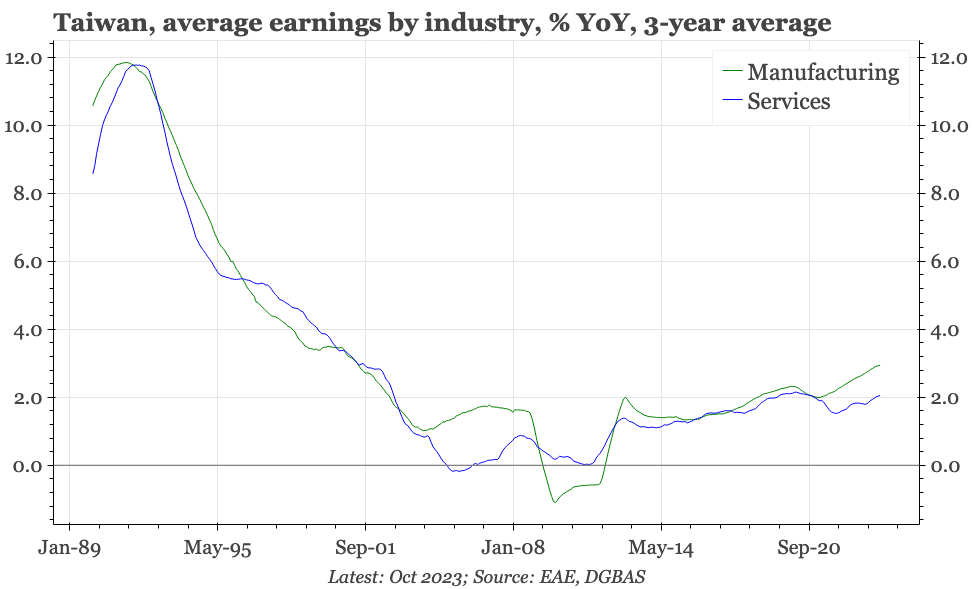

Is wage growth now on the up?

A stronger exchange rate and more generous social spending would help to address some of the economic angst felt by votes. However, it is also true that nominal wage growth has been very low in Taiwan for years. Official data show wages grew by an annual average of just 1.3% in the twenty years to 2020. That helped to anchor core inflation at an average of just 0.4% YoY. From a price and wage inflation perspective, Taiwan is the economy in Asia that has looked most similar to Japan.

With the government in Taiwan – like its counterpart in Japan – being slow to respond to banking sector problems that emerged during the 1990s, this weakness in inflation is partially understandable. Those financial problems have now been resolved. Anyway, in other respects, notably manufacturing productivity, Taiwan's post-1990s experience has been entirely different to Japan's. So there are reasons that wage growth should be stronger, and there are signs that this may be happening. Wage growth has been drifting up, as has inflation, and with unemployment still falling even as Taiwan emerges from the deep export recession of 2022-23, there's room for optimism that both trends can be sustained. That in turn is a pre-condition for interest rates to be higher, which would help to control the property price inflation that is the other usual common gripe of younger voters.

Is the dominance of TSMC good for Taiwan?

Back in 2000, Craig Addison came up with the concept of the silicon shield. The idea was that the importance of the semiconductor sector gave Taiwan a sort of golden goose quality, making China reluctant to invade, and the US more likely to protect. Morris Chang, who founded TSMC in the 1980s as part of Taiwan's industrial policy at the time, has referred to the semi industry as the "sacred mountain that protects the country".

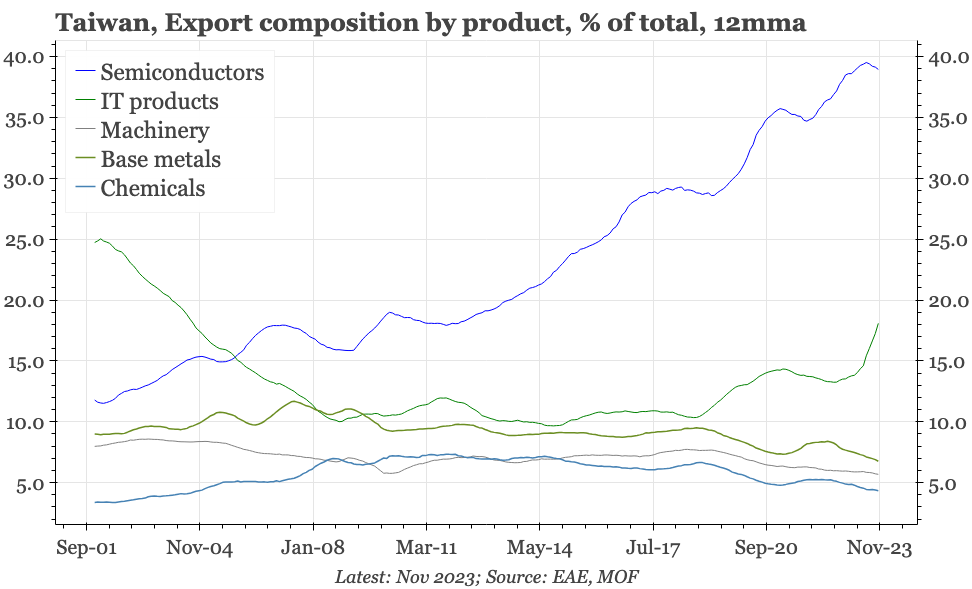

That is all meant from a security perspective, but TSMC in particular has been just as critical for Taiwan's economy. It now accounts for around one third of Taiwan's total market capitalisation and manufacturing capex. 40% of Taiwan's exports are now semiconductors. The growth of the company has been part of the bigger story of the economic development of Taiwan, and isn't something to be regretted. That said, TSMC is now so big that Taiwan's continued economic development increasingly depends on the fortunes of this one company. If I were a voter, I'd want to know happens if and when TSMC's dominance fades, and how presidential candidates are planning for that eventuality.

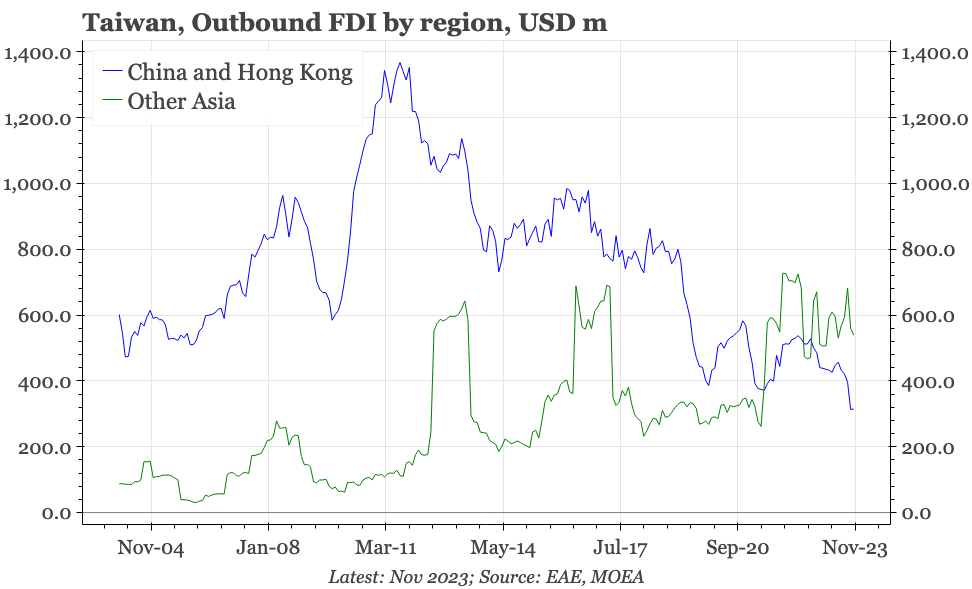

Is economic dis-integration with China risky?

One of the great contradictions of Taiwan – and arguably the reason for the economy's steady development under either political party – has been the disconnect between political and economic relations with China. Politically, Chen Shui-bian was probably the most outwardly pro-independence leader in Taiwan's history, and yet he opened direct cross-Strait travel links, and during his tenure, annual mainland investment approved by Taiwan's government rose from under USD2bn to over USD10bn. When Ma Ying-jeou met Xi Jinping in 2015, it was the first ever direct interaction between the leaders of the Republic of China and the People's Republic of China. And yet, by the time he left office, Taiwanese investment in China had fallen back below USD10bn

Since Ma left office in 2016, that fall has only accelerated. Data for the first 11 months of 2023 show that Taiwan investment in China last year likely fell to around USD3bn, the lowest since 2001. If the KMT wins the presidency this month, them both Taipei and Beijing will try to reinvigorate the relationship, and some change is likely to be seen in services trade. However, the shifts in manufacturing seem much more structural, reflecting global geopolitics, as well as the changing competitive landscape and cost base in China. Perhaps the increasing economic interaction across the Strait didn't play any role in dampening political tensions previously, but the reversal still seems relevant for thinking about Taiwan's future.