Subscribers Only

Last week, next week

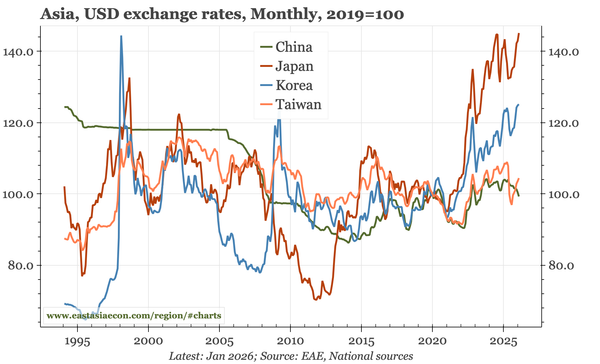

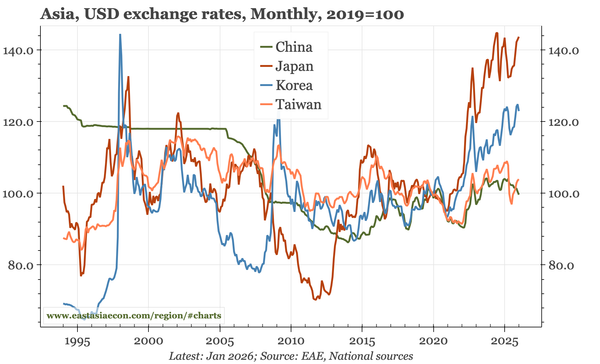

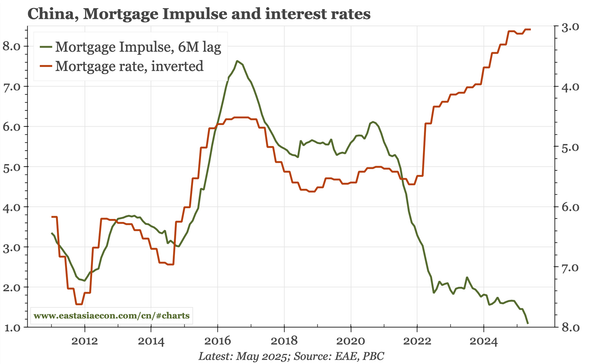

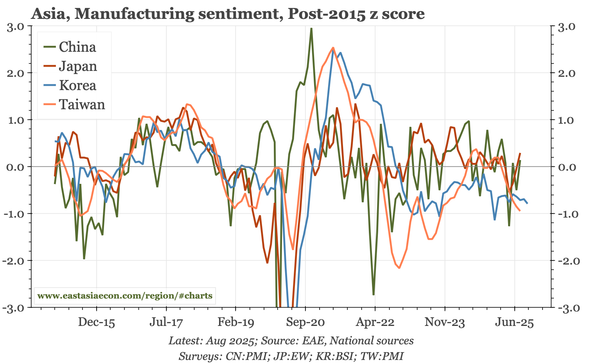

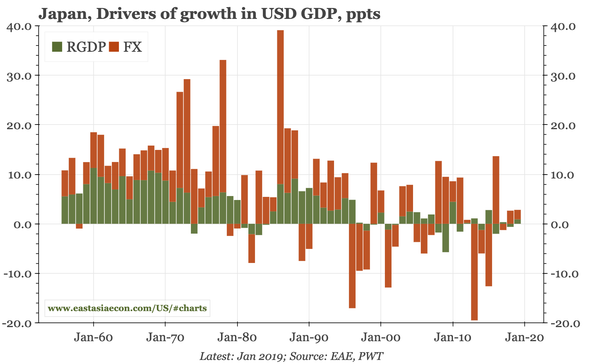

Stabilisation in China seems to be becoming a more popular view. Hope is building for a BOJ hike in June, but one won't be enough. KRW should be strengthening, but likey needs more Middle East certainty. The big event for the region this week is the Xi-Trump meeting.