Subscribers Only

Korea – two warnings about inflation

Yesterday's loan officer survey and today's PPI print both warn about inflation risks. However, in PPI, it is only goods prices that offer clarity. Services PPI has risen too, but seems to suffer from the sort of distortions that are making trends in CPI services inflation difficult to interpret.

Subscribers Only

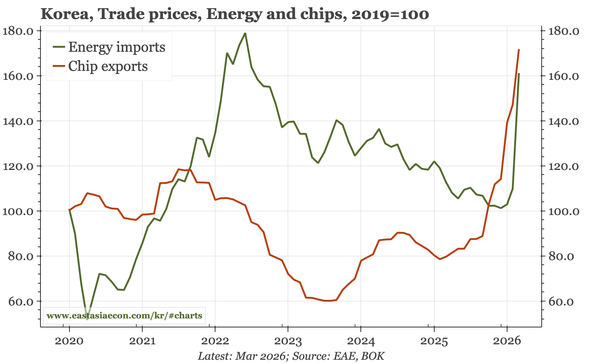

Korea – TOT still up in March

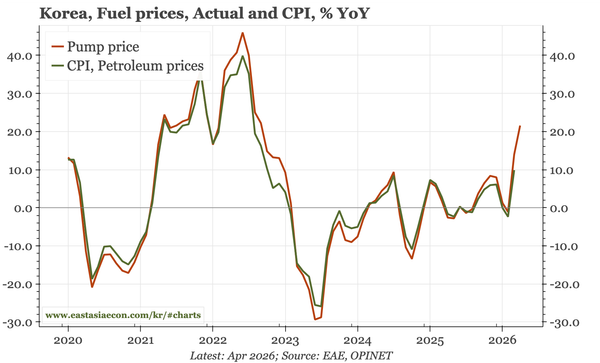

Energy import prices surged 50% in March, and that will undoubtedly raise inflation. However, Korea's terms of trade actually continued to rise (just about), helped by the continued sharp rise in chip export prices. For Korean growth, there is an offset to this energy crisis.

Subscribers Only

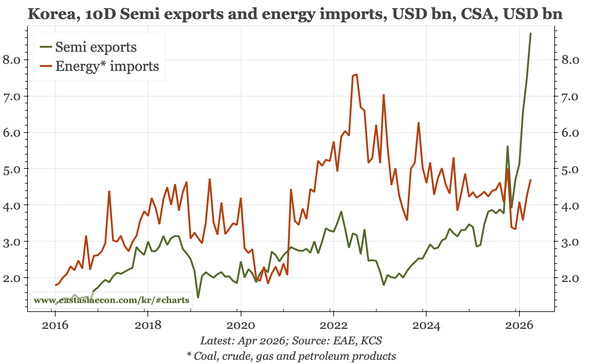

Korea – exports up again in April

Trade data for the first 10 days are volatile. But the April data are still worth highlighting. They show strong exports and a rising trade surplus, which offers a contrast with the BOK's concerns about the cycle, and the market's worries about the KRW.

Subscribers Only

Korea – uncertain, but with conviction

For me, the tone of today's BOK meeting was a surprising mix of uncertainty and conviction. On the one hand, the bank stressed that the outlook is unclear, depending on events in the Middle East. On the other, it seems very sure that inflation will be quite a lot higher than 2%, and growth lower.

Subscribers Only

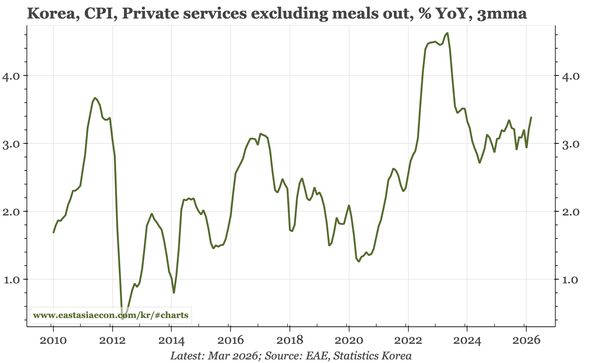

Korea – why is inflation so high?

GDP growth has been below the BOK's estimate of potential almost continually since 2022. And yet core inflation hasn't dropped below target, and private services inflation – a proxy for domestically generated inflation – has picked up to above 3%. Just what is going on?

Subscribers Only

Korea – inflation constrained, for now

Government measures are restraining energy prices and so headline CPI. But the war still increases upside risks for inflation. Rising oil prices are pushing up energy and intermediate prices, export growth is strong, and core inflation has been resilient.

Subscribers Only

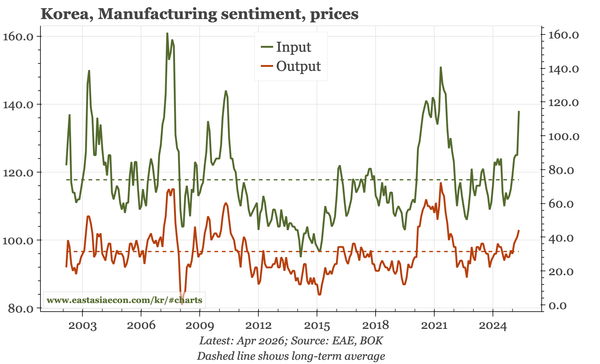

Korea – prices up, sentiment down

The easy takeaway from the rise in prices and fall in sentiment in the BOK's business sentiment survey for March/April is stagflation. I think there are reasons as yet to discount the idea that activity has slowed, but if that is right, then the rise in inflation makes BOK rate hikes more likely.

Subscribers Only

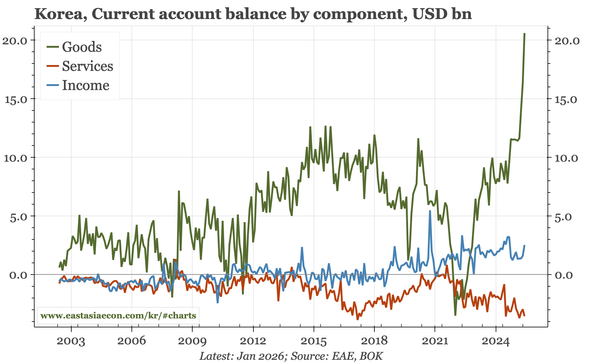

Korea – no change in BOP or CPI...yet

The CA surplus was strong in January, but while NPS outflows eased, retail buying of offshore equities remained high. Core inflation ticked up to 2.3% YoY, but that was related to holiday spending. The impact of the Middle East war will only start to be seen from March data.

Subscribers Only

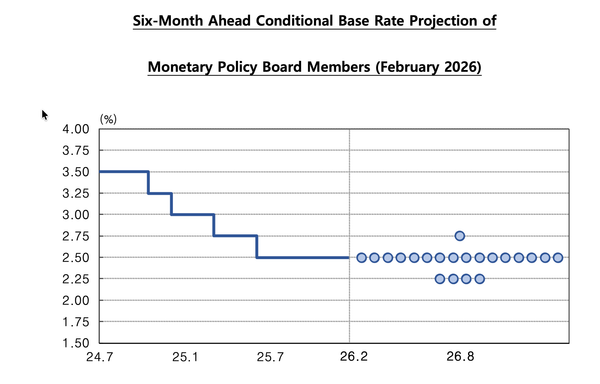

Korea – BOK remains cautious

The tone from today's BOK meeting was cautious. The new rate dot plot suggests that at the margin risks for policy are still weighted towards loosening, the upgrade to the GDP growth forecast was only 0.2ppts, and having made that change, the bank thinks risks to the outlook are now balanced.