Subscribers Only

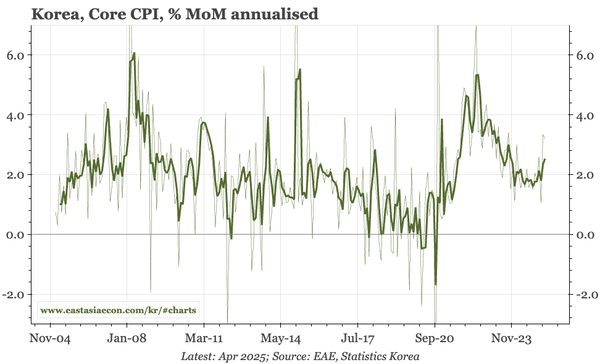

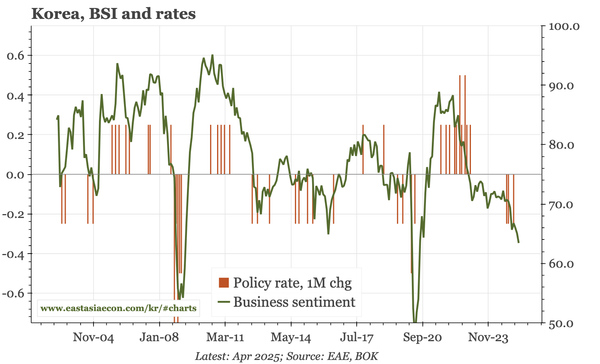

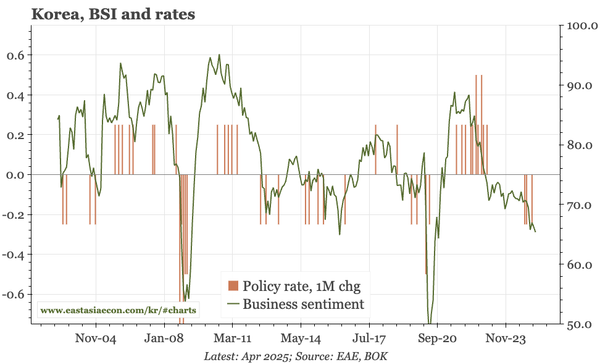

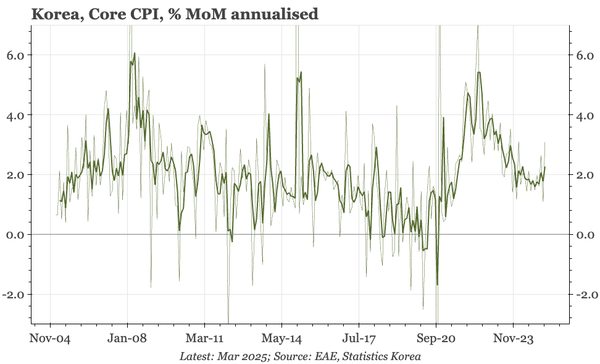

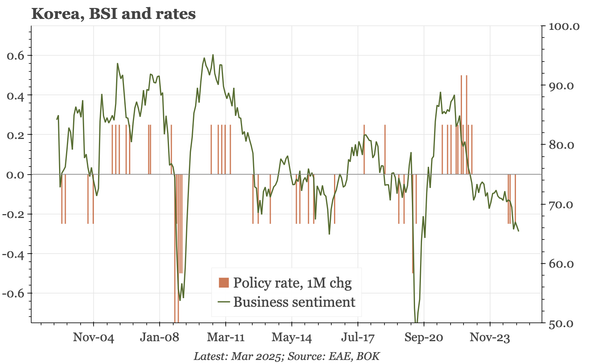

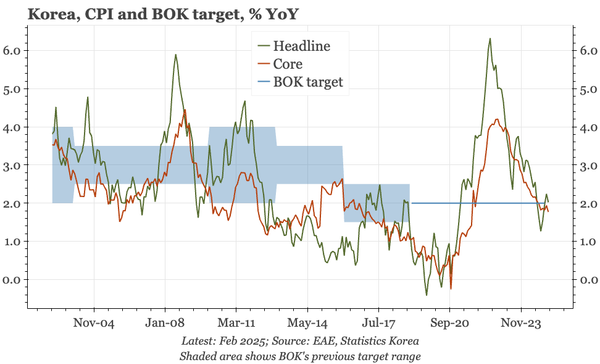

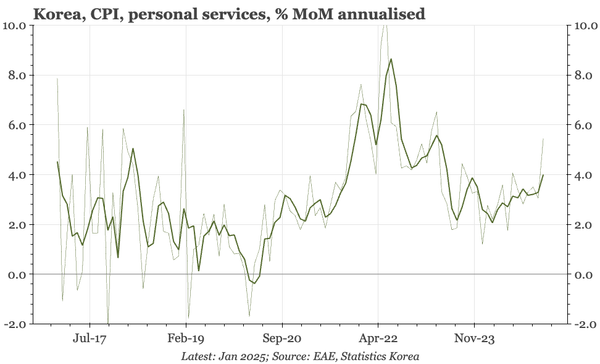

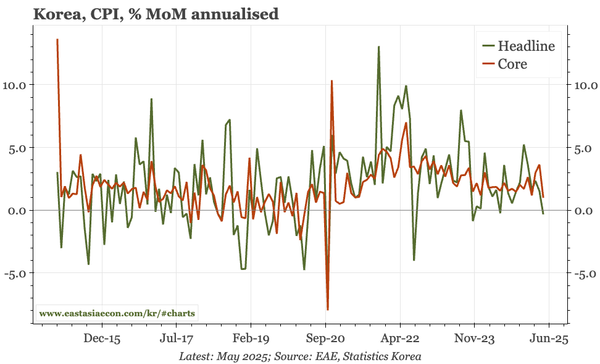

Korea – core CPI lower in May

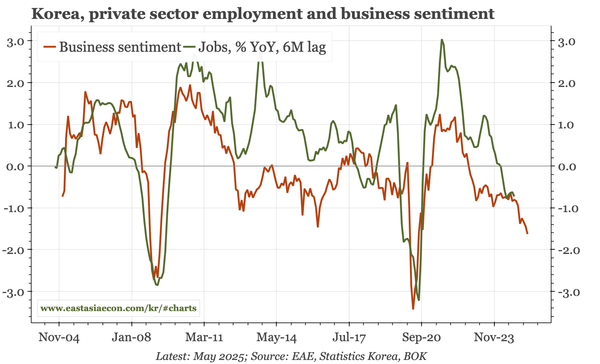

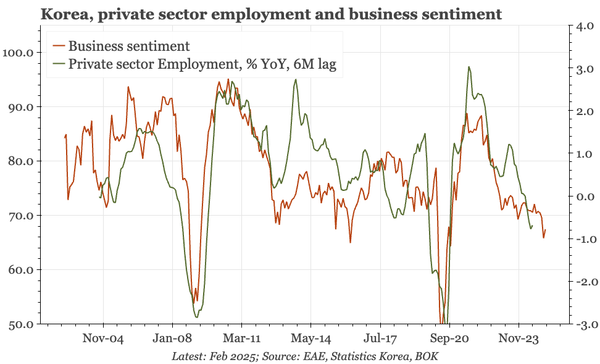

The important detail in today's CPI release for May was the drop in MoM core. Given the weakness of demand – now beginning to show up more clearly in the labour market – that moderation should persist. With global commodity prices weighing on headline, inflation should be less of an issue in 2H25.