Region – import prices up, export prices up more

Data today for Japan and Korea show the inflationary impact of the War, with import prices in both economies rising at double-digit rates. However, such rises have been seen before. By contrast, export price inflation is setting records, offsetting the hit from energy prices to domestic growth.

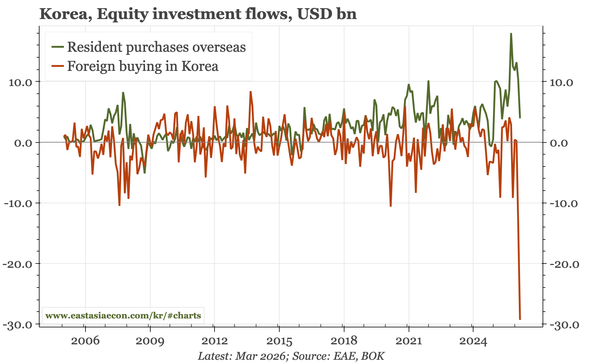

Korea – from foreign buying to foreigner selling

March data offer more evidence that the KRW just can't get a break. Finally, retail outflows into foreign assets eased, only to be replaced by huge domestic selling by overseas investors. That has normalised in April, so perhaps investors are realising that a CA surplus of 20%+ of GDP should matter

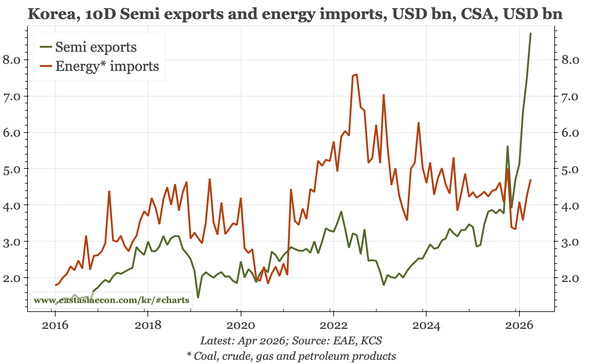

Korea – semi still offsetting energy

The BOK's current forecast assumes no GDP growth in the rest of the year, and contracting exports. But export growth still looks to be picking up, capex indicators are improving, and there is a tailwind from growth in real Gross Domestic Income in Q1 being faster than any time since the 1990s.

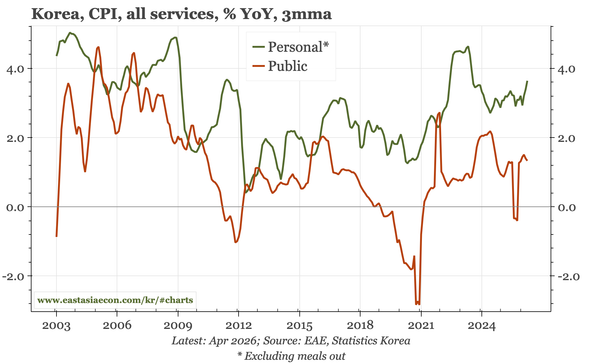

Korea - services inflation still firm

Dearer oil boosted pump prices and so headline CPI in April, but also airline fares and so services inflation. That is another reason to think that personal services inflation of near 4% YoY isn't a true reflection of underlying prices. But it will still matter for the BOK if the chip cycle holds up

Korea – two puzzles

My latest video, discussing two of the issues that puzzle me about Korea: the weakness of the KRW despite surging export growth, and the strength of inflation despite GDP growth – until today – being well below potential.

Korea – inflation, and higher growth

Today's consumer confidence survey warns of higher inflation but slower growth. That is the BOK's base case, and if growth does slow, then there is a reason to look through inflation. But today's Q1 GDP data show much higher growth, boosted by a semi cycle that isn't yet ending.

Korea – two warnings about inflation

Yesterday's loan officer survey and today's PPI print both warn about inflation risks. However, in PPI, it is only goods prices that offer clarity. Services PPI has risen too, but seems to suffer from the sort of distortions that are making trends in CPI services inflation difficult to interpret.

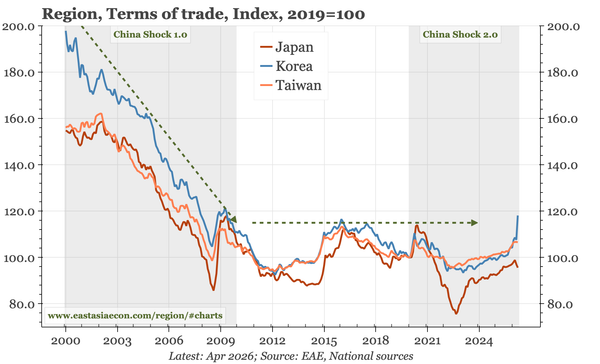

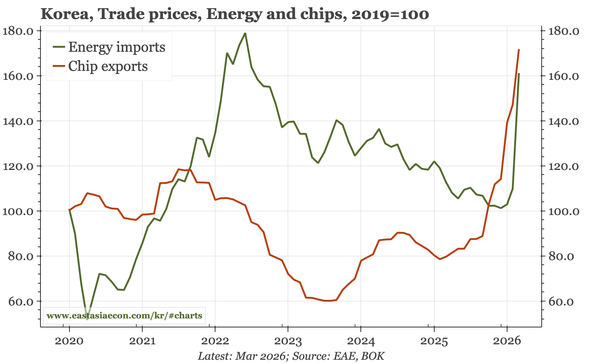

Korea – TOT still up in March

Energy import prices surged 50% in March, and that will undoubtedly raise inflation. However, Korea's terms of trade actually continued to rise (just about), helped by the continued sharp rise in chip export prices. For Korean growth, there is an offset to this energy crisis.

Korea – exports up again in April

Trade data for the first 10 days are volatile. But the April data are still worth highlighting. They show strong exports and a rising trade surplus, which offers a contrast with the BOK's concerns about the cycle, and the market's worries about the KRW.