Members Only

Region – China and 1990s Asia

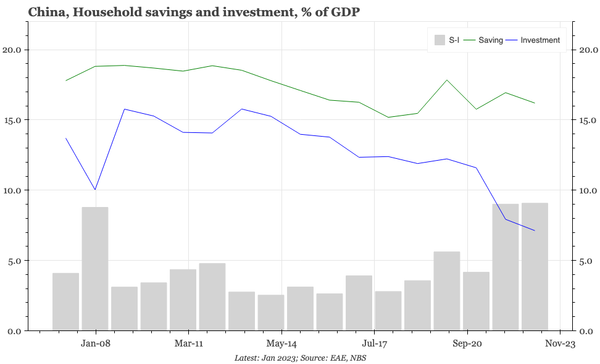

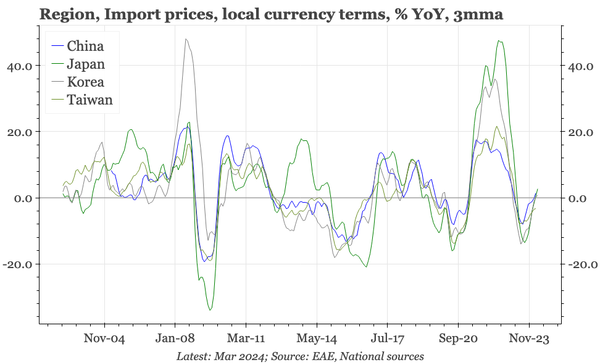

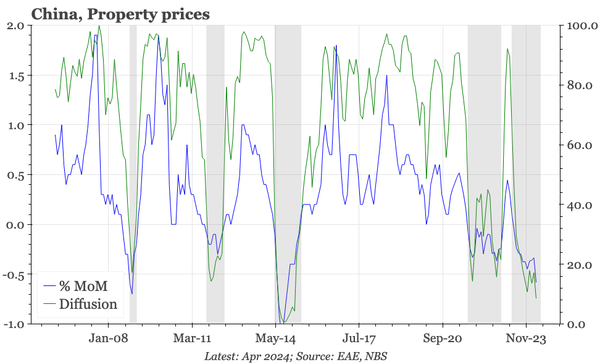

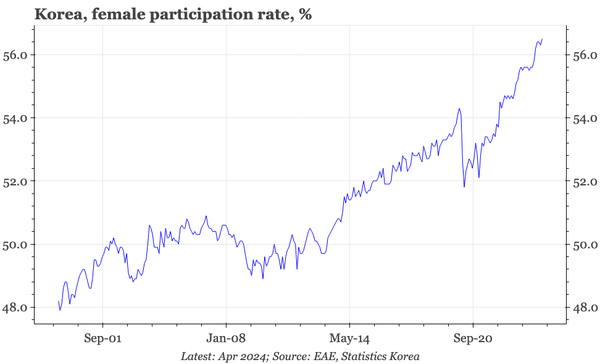

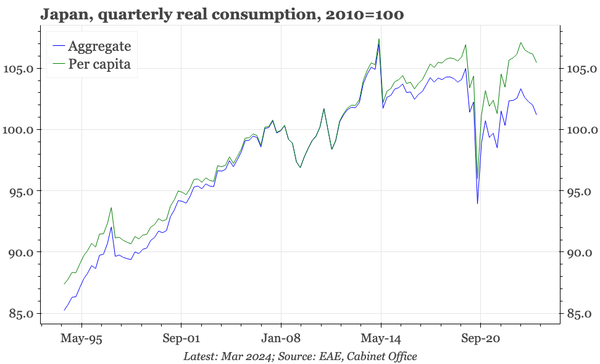

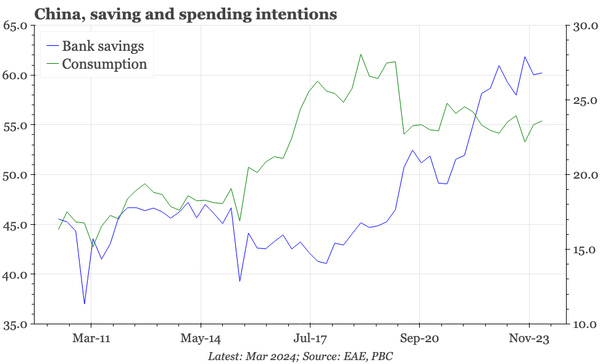

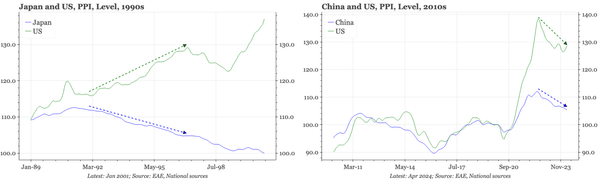

A refreshed slide pack looking at China today and the experience of Asia in the 1990s, with a focus on deflation and rates, exports and mfg, and household income and consumption.