Subscribers Only

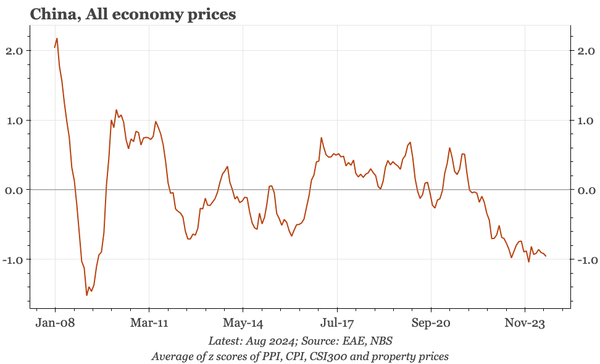

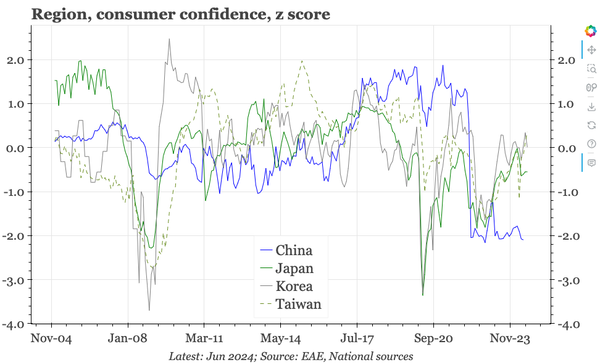

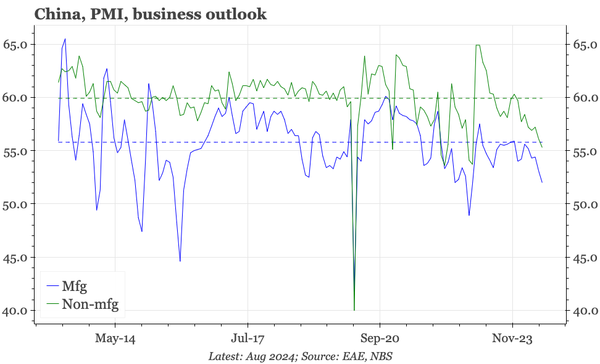

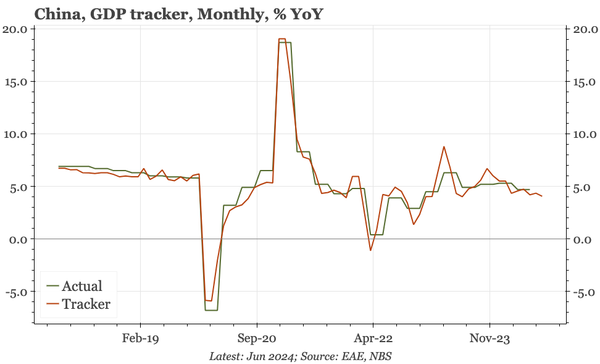

China – GDP growth tracking 4%

August data suggest GDP is now only growing by around 4% YoY. The headwinds remain property activity, which dropped again in August to new lows, and retail sales, which has now contracted MoM in five of the first eight months of 2024. Sustaining muddle through is getting much more difficult.