Subscribers Only

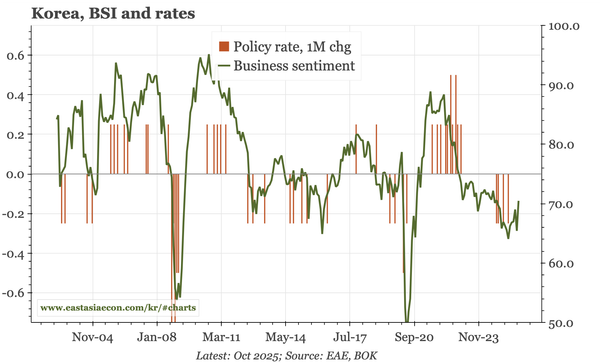

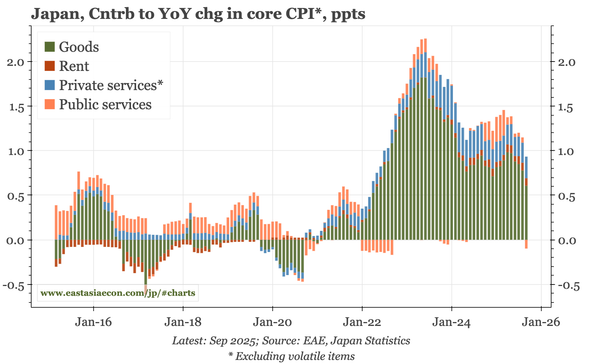

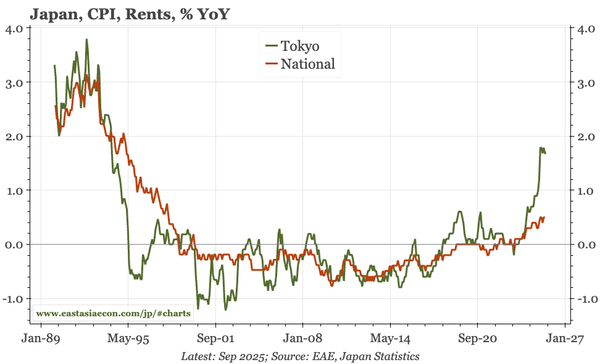

Japan – Board thinks the time for another hike is getting closer

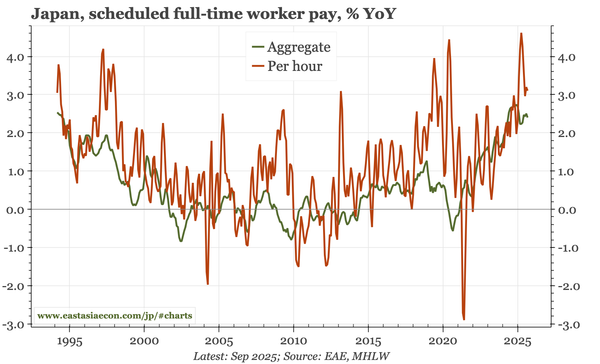

The summary of the October BOJ meeting show a stronger consensus that the time is approaching for another rate hike. That is partly because concern about tariffs is fading. It is less about domestic demand: data today show consumption trending up, but still only very slowly.