Subscribers Only

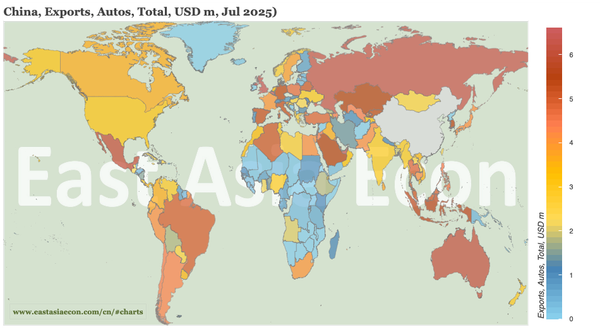

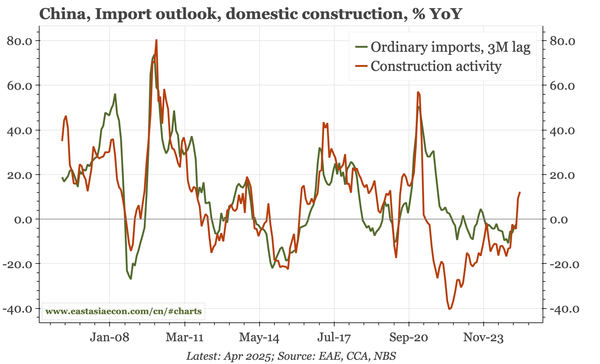

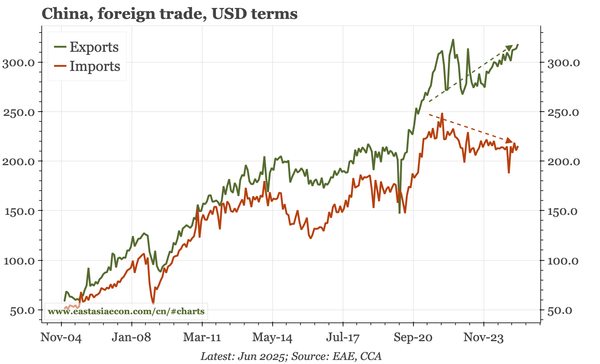

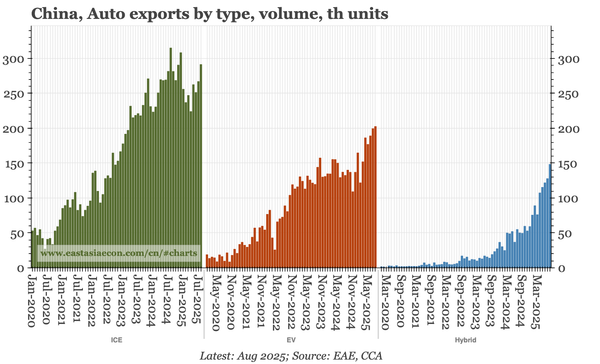

China – auto exports accelerating

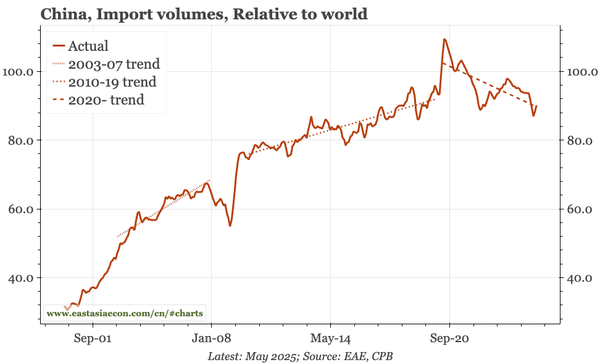

China's trade data are published over the course of four releases each month. We are now onto the second, with three main takeaways: auto exports are accelerating again, import demand is up, and the trade surplus continues to broaden.