China - weekly update

The government's plan right now is to get the virus under control, and then guide companies back to work, thereby lifting the economy out of the covid shock without having to commit to a whole load of new 'stimulus'.

Someone in the policymaking establishment in Beijing seemed to decide quickly that the 25bp cut in the reserve requirement ratio on Friday last week didn't send quite the right message. Yesterday the PBC implied that in fact it had effectively cut by 50bp, stating that the CNY600bn in profits it has handed over to the government so far this year was equivalent to another 25bp reduction in the RRR.

These profit transfers are - or at least should be - a theme for this year, with the ministry of finance already saying that the 2022 budget would be financed in part through transfer of these accumulated earnings from state-owned units to the government. To the extent that this continues to unwind the considerable fiscal deposits that have accumulated at the PBC, would represent both a fiscal and monetary easing, an improvement in the financial efficiency of the state sector, and would also imply less credit growth will be needed to achieve the 5.5% growth target.

The budget, and the growth target, were however announced before covid started to spread again. The shock to the economy from the lockdowns that are being used to try to once again stamp out the virus would suggest that more policy easing will be needed that the previously-planned fiscal measures and recent modest monetary easing. The State Council itself has talked about the need for more "urgency", but so far, the biggest change has been the Friday RRR cut.

The statement from the PBC yesterday looked impressive, including a list of 23 measures, but they didn't include big, specific new commitments, rather reiterating the cyclical policy direction of the last few months (for example supporting the "reasonable" demand for liquidity from homebuilders and construction firms) and continuing with policies initially used when the economy was first hit with covid (such as rolling over the re-lending scheme for small firms).

It seems the government's economic thinking for now involves two parts. First, that, like 2020-21, it will quickly get virus under control, and then guide companies back to work, thereby lifting the economy out of the covid shock without having to commit to a whole load of new 'stimulus'. So, there's a plan for Shanghai to achieve "societal zero-covid" - meaning new cases are found only among people already in quarantine - by tomorrow. As for getting companies back to work, the PBC's 23 measures are related to that, as was a meeting yesterday chaired by vice premier Liu He and called to clear up supply-chain snags caused by covid.

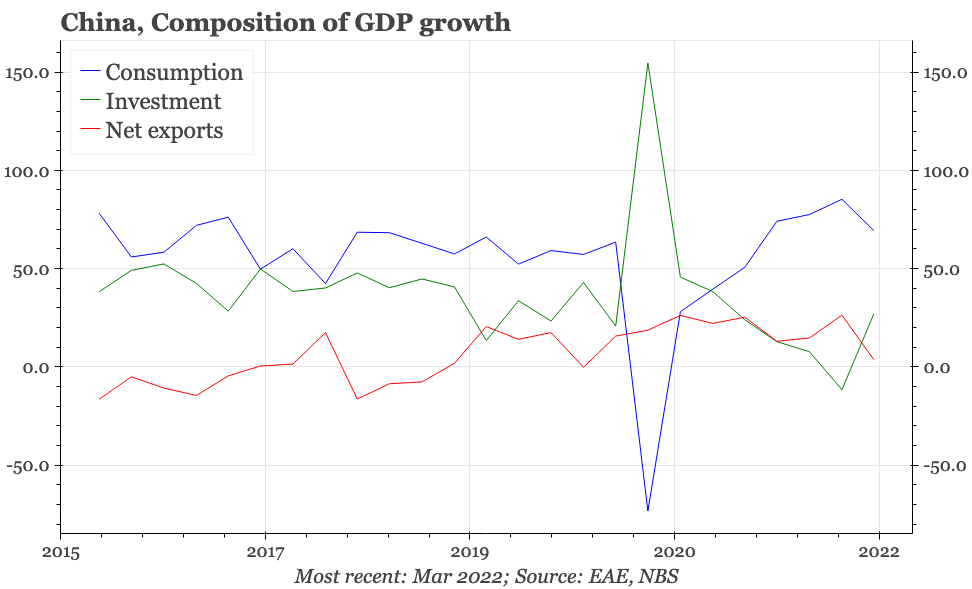

The second part of the strategy is that the shift in cyclical policy that has slowly emerged since September last year will continue to show up in the data as it did in Q1. Thus, the surprisingly strong GDP growth for January-March that was announced yesterday was driven by rebounds in construction and fixed asset investment, seeming to show that recent increases in infrastructure spending and efforts to stabilise property are having an impact.

The problem is that official GDP data for the whole of Q1 aside, there aren't strong signs that the tentative bottoming of the construction cycle that was taking shape is surviving the latest covid shock. The signs of a turn better in property construction and sales faded in March, and excavator sales, which had shown signs of improving, also relapsed during the month.

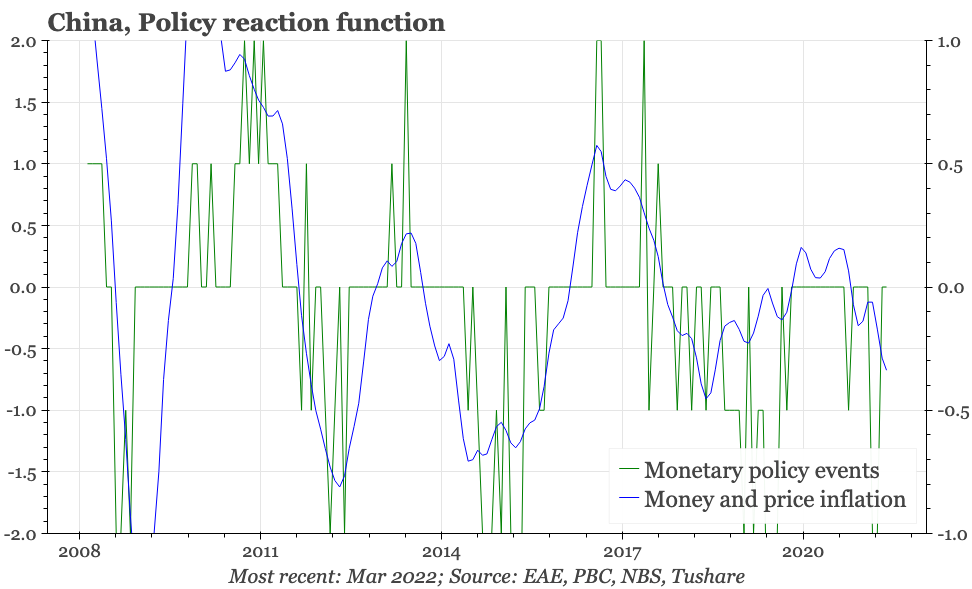

This suggests that policymakers are going to have to do more, and here they do have some options. It has been surprising that rates haven't been cut more, but in its recent statements the PBC has said that actual interest rates for the real economy have fallen a further 20bp in then last three months to a new record low. There's analyst talk of monetary policy being constrained by inflation and currency weakness. The global inflation picture may be a concern, but overall monetary policy moves don't look out of whack compared with the generalised easing of domestic inflation. As for the currency, while there are signs of capital outflows, which likely will intensify, to some extent those should be welcomed given that from the point of view of the domestic cycle, the CNY if anything looks to be too strong.

If the government doesn't feel it can do much on the monetary front and needs to look for some new way to boost the economy, then there is an ideal candidate in the form of domestic consumption. The household sector has now been depressed for two years, with income growth of just 5.4% YoY in Q1. The direct reason for the softness in consumption is of course the economic restrictions caused by covid, and sometimes fear of the virus itself. That backdrop means the efficacy of any support for the consumer is linked with the government's overall attitude towards covid. Needless to say, Beijing shows no signs right now of being willing to "live with the virus". But frankly, even if if was, the bigger obstacle to a consumer stimulus is it just doesn't seem to be the way policymakers in China think. If there is a major consumer package in the works, if there will be a big - and positive - surprise.

If the government isn't willing to switch approach and boost consumption, then it has two further options. One is simply to give up on growth this year. It does have the excuse of covid, but still, this doesn't seem like the most obvious path for officials to take. Policymakers have been saying it is important to retain confidence in the economy, which would seem more difficult to do if the government itself was messaging that the cycle was in trouble. There's also political demands for stability in the run-up to the 20th party congress later this year, a consideration which is now being explicitly mentioned in policy statements, including that issued from Liu He's logistics meeting yesterday. More generally, continued economic development is a key part of the CCP's long-term aims for the country.

That leaves one more option, which has been mentioned in the policy debate - a 1998-style issue of special government bonds. That seems possible, and it is conceivable that the money raised could be used in part to fund some kind of help for the consumer. More likely though would be for Beijing to double-down on the current investment-led strategy.

More comprehensive China charts can be found here.