China – watching what to watch

A few weeks ago, we laid out a list of indicators to be watching to track whether all the policy announcements from China were generating a turn in the cycle. Looking through that list now, and it remains difficult to feel excited that they have.

This note from late September identified five indicators to be watching for early signs that China's policy push was gaining traction. This is how those indicators have fared since:

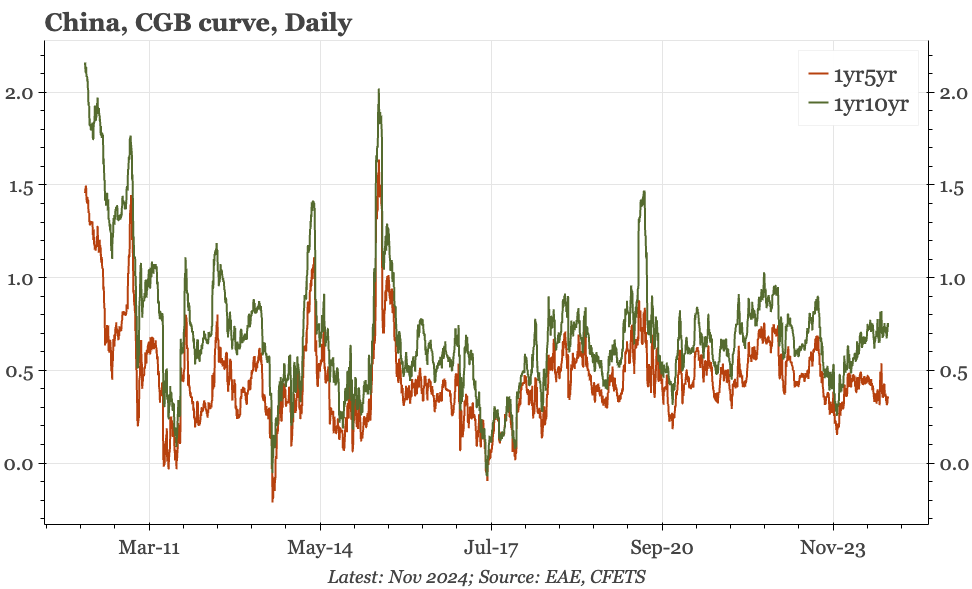

Yield curve. 1yr5yr, which is the most liquid part of the curve, hasn't steepened at all.

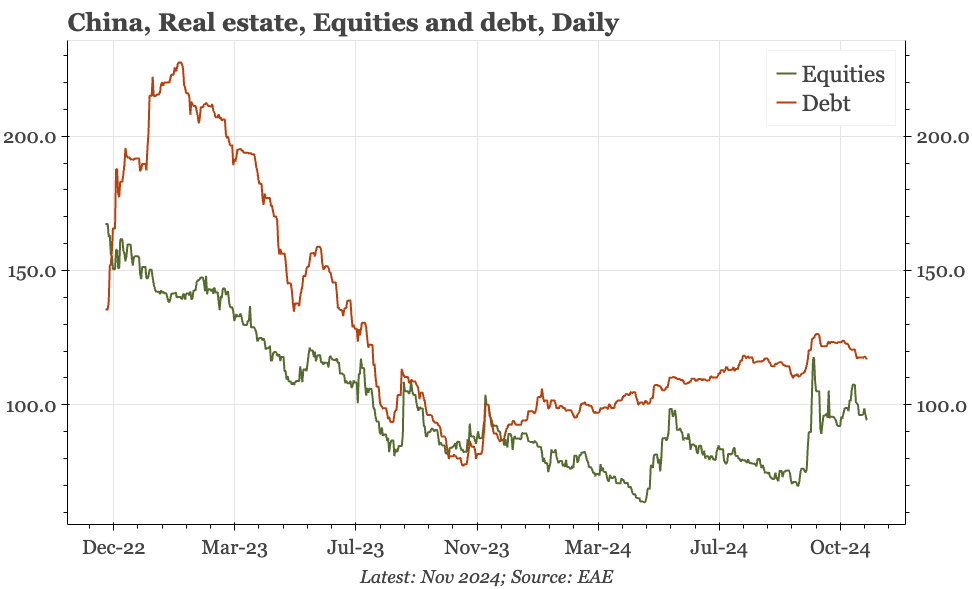

Real estate equities and debt. 3001.hk shows high-yield debt drifting back down to the level of July.

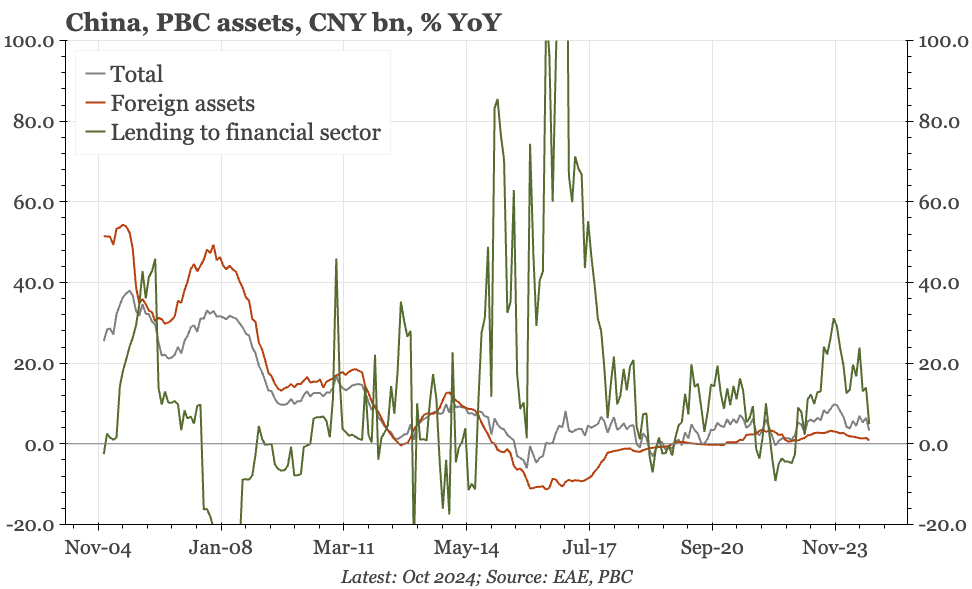

Base money. No acceleration through October, and PBC lending to the financial sector particularly weak.

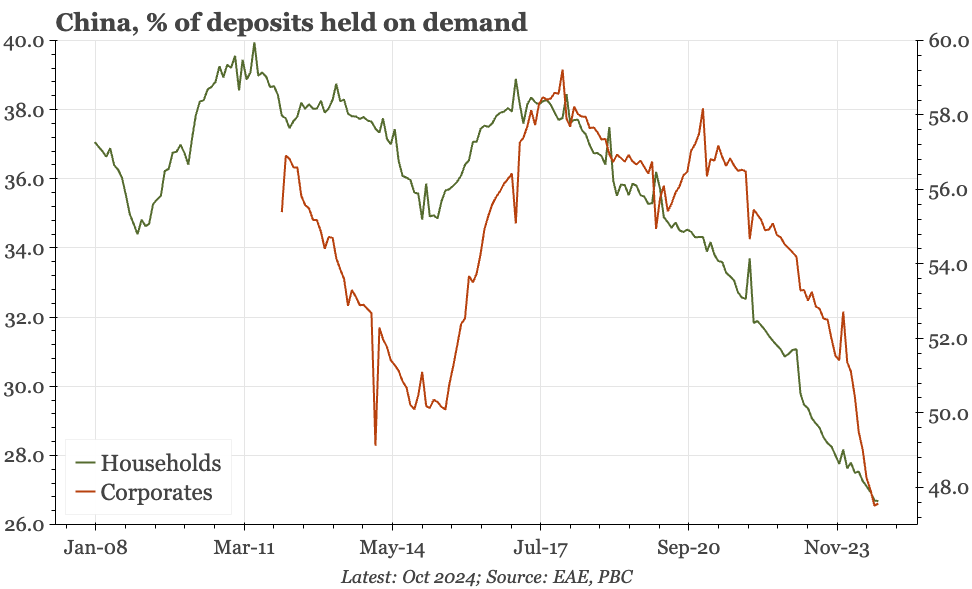

Time deposits. No worsening in liquidity preference in October, but that follows the sharp fall since 2023.

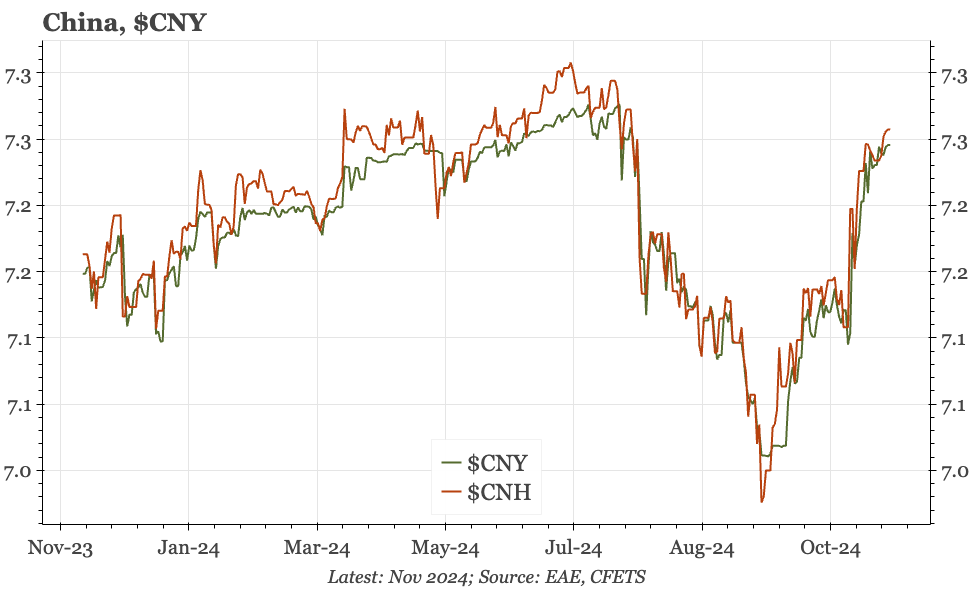

CNY. The currency has given up almost all the post-July gains. Obviously, a lot of that is driven by US events. But US politics and economic policy will not make things easier for China from here.