China – net exports boost growth China doesn't release detailed GDP by expenditure data, but the available snippets show Q1 outperformance was due to net exports.

China – savings rate falling Consumer sentiment does remain low in China, but it is encouraging that income growth has picked up, while the savings rate is coming down.

China – property activity falls even further There's just no floor for property. Starts fell again in March and are now 65% below the 2020 peak, and barely above the low of late 2008.

China – the gap in metals prices There's a growing divergence between ferrous and non-ferrous metals, and that shows the contrast between weak property and strong manufacturing activity.

China – official property px no worse Official data show property price deflation isn't worsening. Private measures suggest the same thing, though anecdotes suggest actual market conditions are much weaker

Region – import px disinflation ending Korean data today continue the clear turn in regional import prices of recent months. This will matter for inflation, even in China.

China – PBC prudence Today's PBC action to drain liquidity for the second consecutive month via the MLF follows a big run-up in 2H23. Still, it does show that the bank remains a cautious easer.

Japan – machine orders still subdued The BOJ uses machine orders as a lead for machinery investment. Data show Feb was stronger, but not by enough to lift the 3mma by much.

Taiwan – wage growth holding up Wage growth did slow in 2023, but that looks cyclical, not breaking the higher rate of trend growth that's been apparent since the pandemic.

China – mortgage lending bottoms out We can be increasingly confident that mortgage lending has bottomed out. But there aren't any signs of a rebound.

China – strong exports in March Exports rose MoM in March, while imports were weak. Outside concern about China's trade surplus is going to intensify.

Japan – happier households Today's Q1 BOJ consumer survey shows sentiment about income rising to the highest level in 20 years.

Korea – the ageing workforce Demographics are really having a big impact on the composition of employment.

Korea – labour market still tight Data today show Korea employment did tick down in March, but the unemployment rate remaining below 3%, the lowest since the 1990s.

China – no inflection yet in PPI China should be close to an inflection in PPI, but the turn didn't happen in March. PPI fell 2.8% YoY, a rate of deflation that hasn't changed much since August 2023.

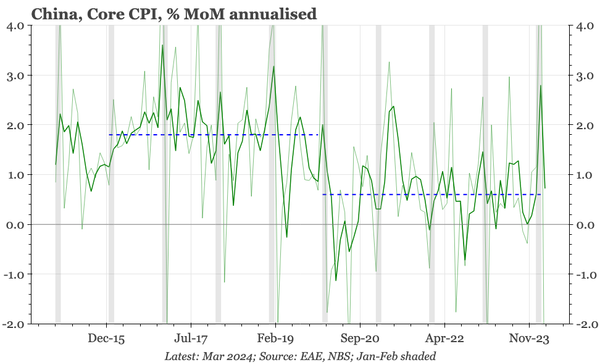

China – core CPI weak, but not negative The pick-up in core CPI from late 2023 hasn't persisted, dropping back to +0.7% in March. That is consistent with the post-covid performance, and a step down from the pre-2020 average of nearly 2%.

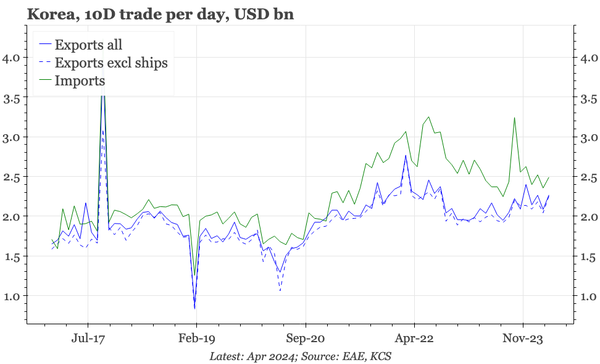

Korea – no change in export momentum Data for the first 10 days of April don't show an acceleration of the mild export recovery of the last few months. That matters for the BOK when domestic demand is also weak.

Taiwan – nominal exports still so-so YoY export growth did accelerate in March to almost 20%, the highest since early 2022. But in level terms, the recovery remains rather sluggish.

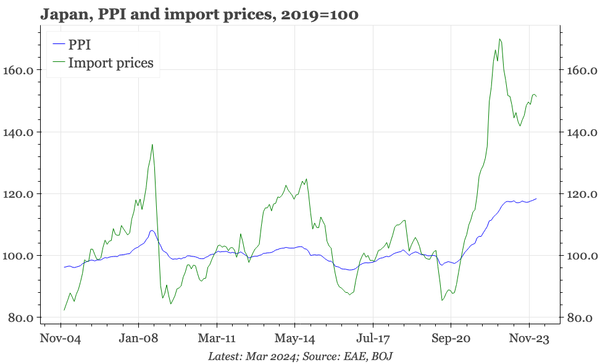

Japan – upstream prices still high If there was supposed to be goods price disinflation in Japan, it didn't last long, and didn't make much difference to the level of either import or producer prices.

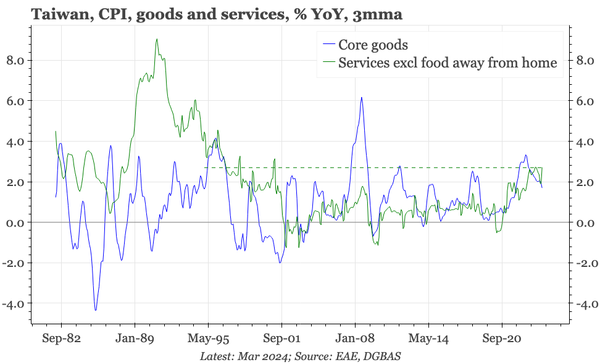

Taiwan – highest services inflation since the 1990s Even after a deep and long export recession, services inflation in Taiwan is still running at the highest rate since the late 1990s.

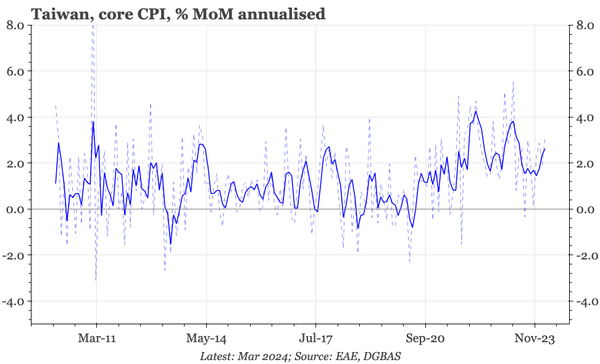

Taiwan – core inflation re-accelerates Data today show core CPI inflation accelerated to an annualised 3% in March. No wonder the central bank raised rates last month.

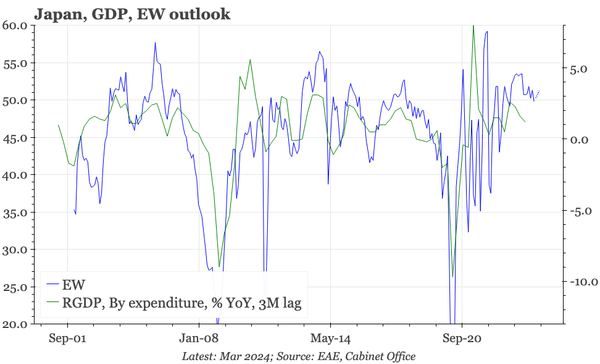

Japan – cycle retains momentum The EW survey in March fell MoM, but remains well above the long-term average, and continues to point to better GDP growth.

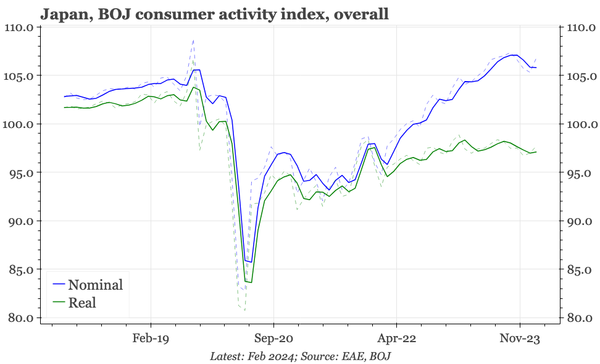

Japan – no consumer rebound yet As in China, consumption has been the big macro drag in Japan. That should change in 2024, but BOJ data through February show no turnaround yet.

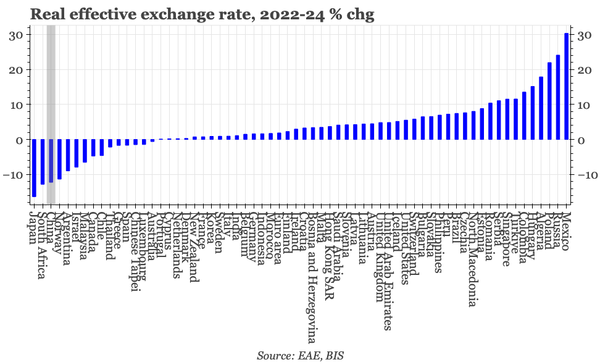

China – few currencies weaker With a weak cycle, policy is being loosened. But given China's obvious industrial strengths, it is still striking how much the CNY has weakened.

Japan – output gap closes Japan's negative output gap has finally closed! But that has taken 14 quarters, and even now, the BOJ calculates the positive output gap is just 0.02%.