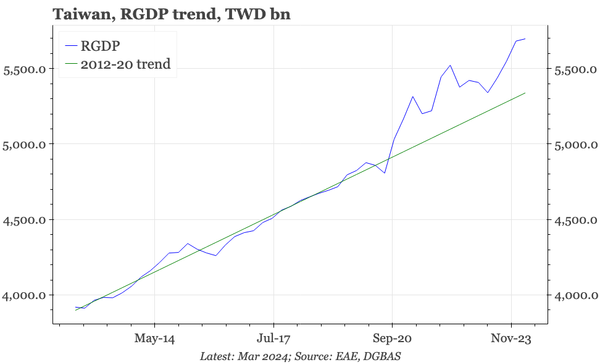

QTC: Taiwan – stronger since covid Taiwan must be about the only economy where covid provided a big boost to GDP, a lift that today's Q124 data show once again isn't disappearing.

QTC: Japan – inflation erodes confidence again Consumer confidence for May has the same message as the earlier EW survey: the weaker JPY and rise in goods prices is once again eating into real incomes and eroding consumer confidence.

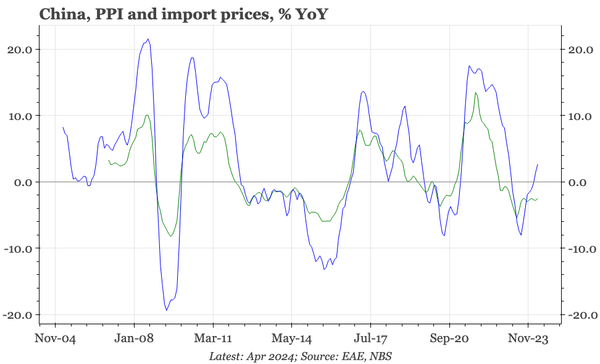

QTC: China – rising import prices suggest PPI rebound Import prices rose for the second consecutive month in April. It will be a surprise if domestic PPI inflation doesn't now follow suit, and in so doing challenge the idea that China is stuck in deflation.

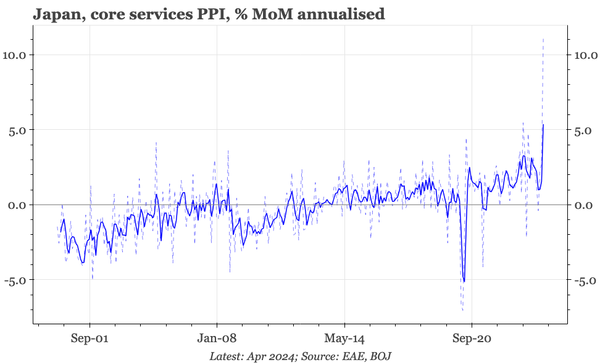

QTC: Japan – strong upstream services inflation Services PPI has been one of the best indicators of Japan's structural exit from deflation. The slowdown from mid-2023 had thus been concerning. But a rebound started earlier this year, and today's release for April was very strong.

QTC: Taiwan – no consumer slowdown Domestic activity carried the economy in 2022-23 as exports slowed. Exports are now picking up, but consumption is also remaining solid. Consumer confidence isn't particularly strong, but purchasing intentions are.

Japan – BOJ still confident The summary slide from BOJ Uchida's speech today is complex. The last line of the text was clearer: 'I would like to conclude my speech with this phrase: “This time is different.”'

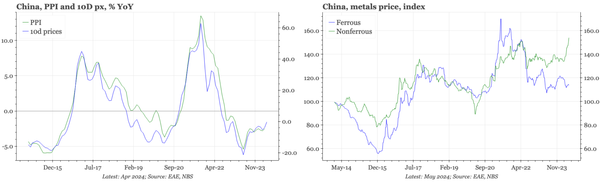

China – PPI turning up High-frequency data continue to show a lessening of upstream deflation, though the change is being disproportionately driven by copper prices.

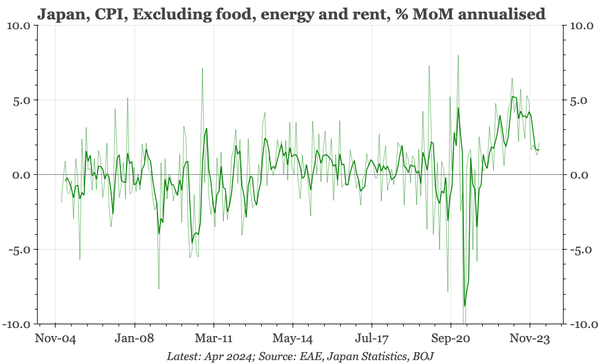

Japan – underlying inflation ticks up The uptick in underlying inflation in April wasn't much, but is still important, as it fits with the BOJ's idea of transition from import prices to services prices.

Taiwan – exports catch up to domestic demand Covid disrupted the usual synchronisation between exports and domestic demand. Recent resynchronisation is positive for the outlook, happening not by domestic demand slowing, but exports picking up.

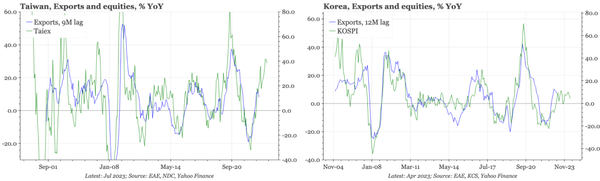

Region – what equity markets are pricing in for exports Updating these charts after Nvidia's results. Semis account for almost 50% of Taiwan's exports, compared with 20% in Korea. For now, that looks like a good dependence to have.

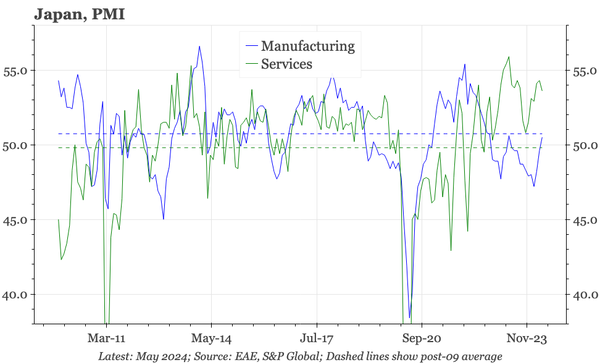

Japan – cycle still solid At 53.6, S&P's flash services PMI for May dipped a little from April, but remains well above the long-term average of 49.8. At the same time, the mfg PMI rose above 50 for the first time in a year.

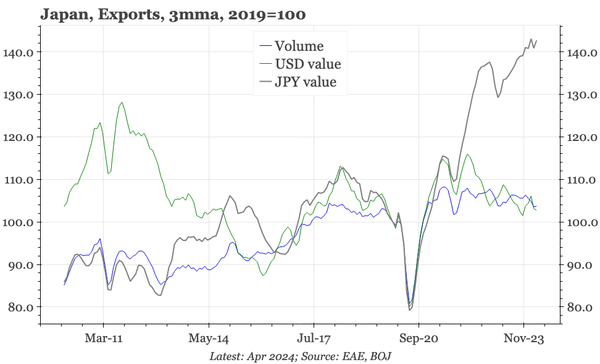

Japan – strong exports, but only in nominal terms Firms still aren't using the weak JPY to cut USD prices and increase volumes. Instead, the ccy weakness continues to flow straight into JPY earnings

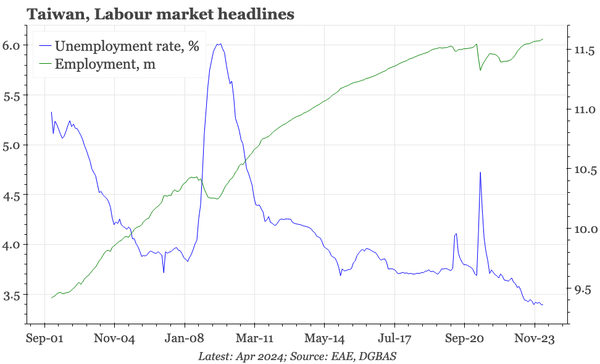

Taiwan – employment still rising Employment rose to another all-time high in April, keeping unemployment below 3%. This labour market tightness is striking when the mfg PMI has been below 50 for most of the last 2 years.

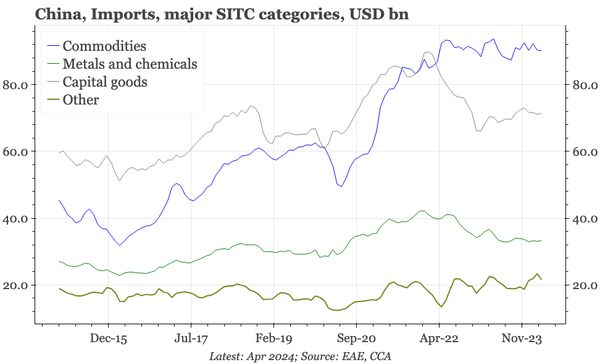

China – only importing commodities You might think that with property activity collapsing and a mfg boom, China would import fewer commodities and more capital goods. But what's actually happened is almost exactly the opposite.

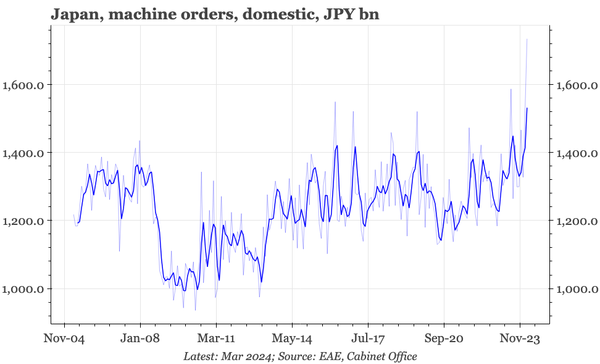

Japan – domestic strength Data today continue the theme of export sluggishness v domestic strength. Exports underwhelmed in April, but the post-covid pick-up in domestic machine orders continued through March.

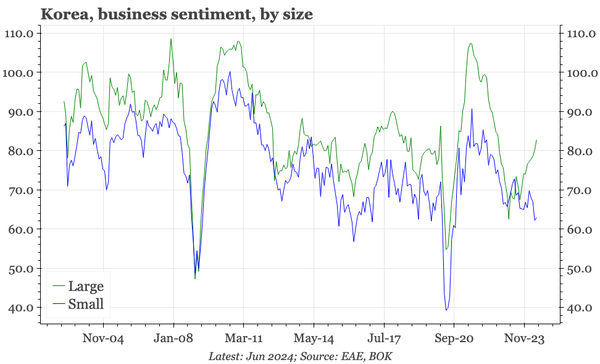

Korea – only good for big firms Chaebol dominance isn't new. But at least cyclically, what's good for large firms usually lifts the small too. But that hasn't been true in 2024, and the gap complicates the BOK's task.

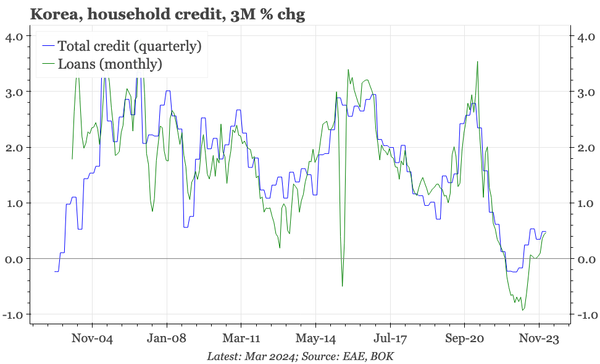

Korea – borrowing growing, but slowly Household borrowing is consistent with the BOK's on-off contention of a soft landing. It is now rebounding, but much less quickly than it was growing before 2020.

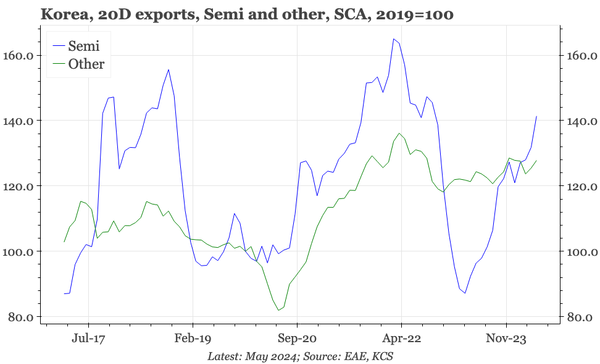

Korea – exports stronger, but only semi Export performance has been stronger in May. Workday-adjusted growth in the first 20 days was almost 20% YoY, a recovery that continues to rely solely on semiconductors.

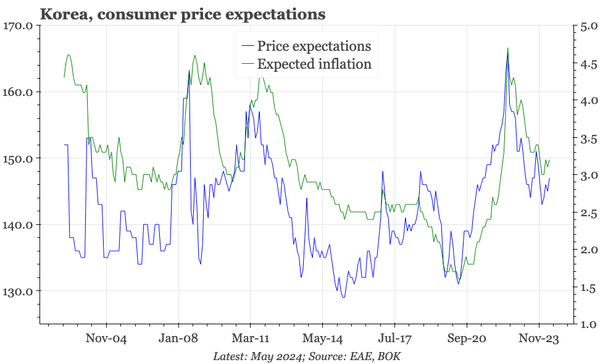

Korea – inflation expectations up Consumer confidence fell in May, which would reinforce BOK concern about domestic demand. But the bank seems stuck for now because inflation expectations also rebounded.

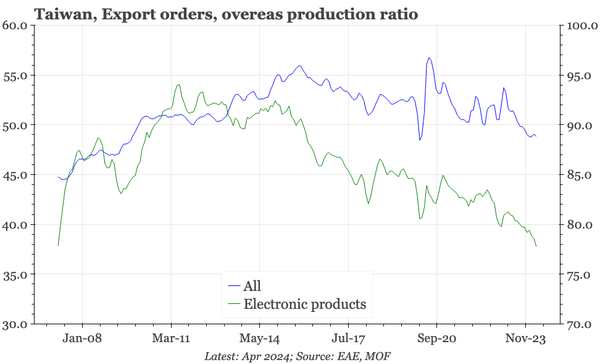

Taiwan – export orders also better Export orders rose in April, but continue to trail actual exports. One reason could be supply-chain restructuring, shown by the fall in the overseas production ratio.

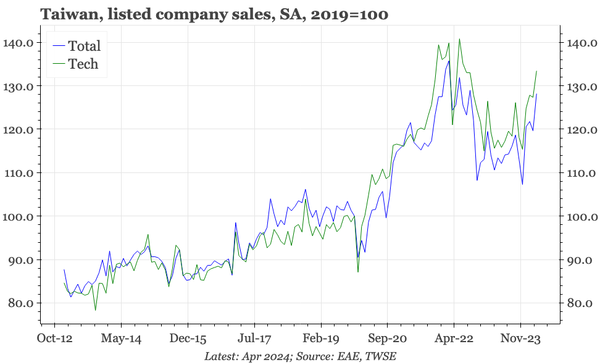

Taiwan – better sales in April This year's expected manufacturing pick-up has been patchy, but perhaps that is changing, with much stronger listed company sales in April, led by tech.

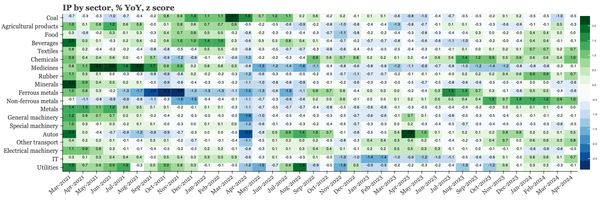

China – broad-based pick-up in IP growth IP growth remains the bright spot in China's economy, with the pick-up in April being broad-based across industries.

China – no turnaround in all-economy prices Today's property price data for April weakened again. With PPI and CPI remaining weak too, the bounce in equity prices hasn't been enough to change the all-economy rate of deflation.

China – still expecting PPI to rebound The April PPI data were soft, but the government's higher-frequency series for industrial prices, updated today for the first 10 days of May, continues to suggest a lessening of deflation.

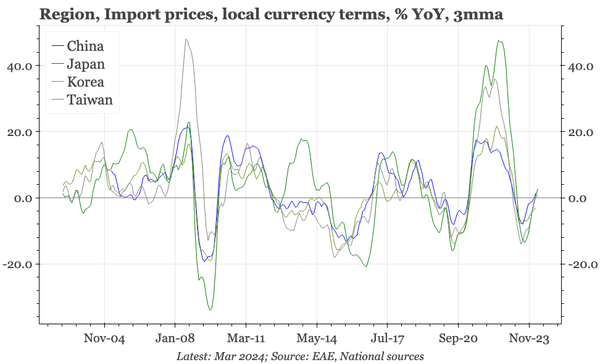

Region – import price inflation returns External goods price disinflation is now over, with import prices now rising again across the region. That is likely to feed into stronger PPI, even in China.