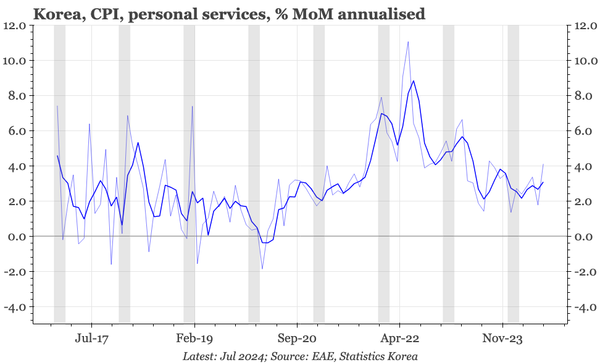

The BOK's BSI survey ticked down in August, but not in a way that changes the picture. The cycle has been weak enough to justify rate cuts for a while, with the hold-ups being CPI, the Fed and, occasionally, domestic housing prices. Currently, it is only housing that is flashing red.