Subscribers Only

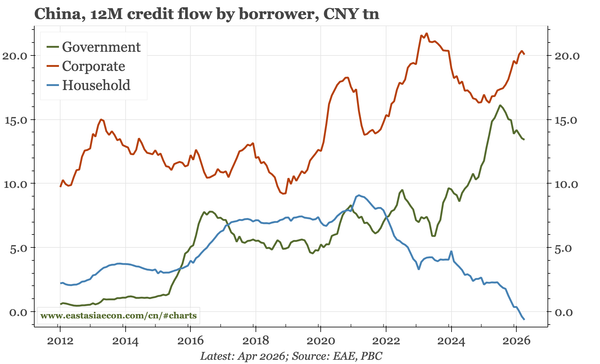

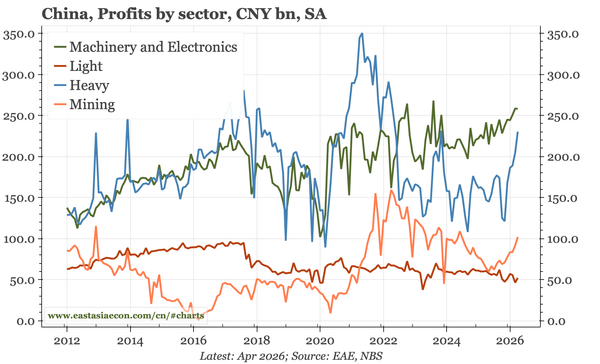

China – underlying profits a bit better

The bounce in headline profits in April was largely base effect, but there are signs of underlying improvement: revenues have started to rise, the increase in PPI is boosting profits in heavy industry, and hasn't yet derailed the post-2024 increase in total downstream manufacturing earnings.