Public Post

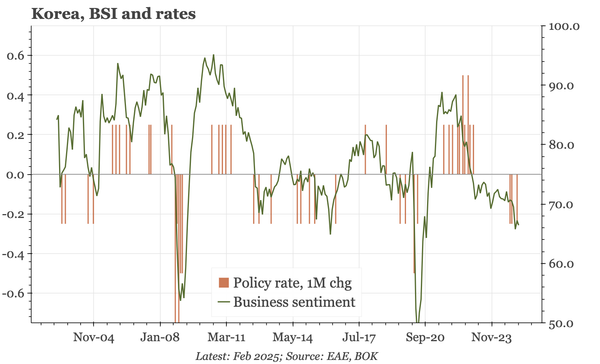

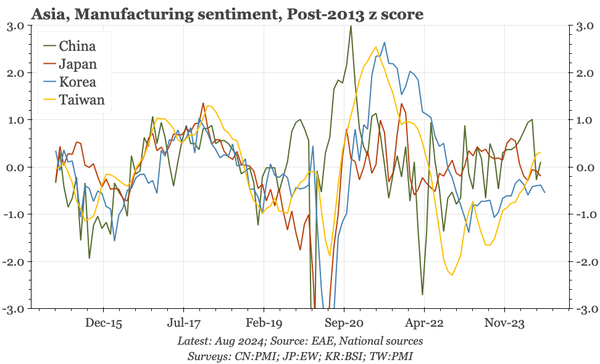

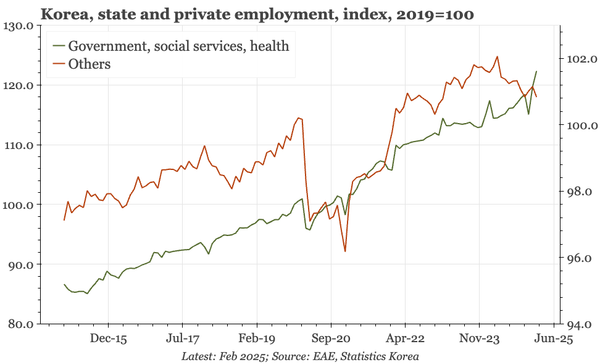

Korea – private sector employment still weak

The reversal of December's fall in jobs continued in February, but the rise is still being driven by employment in the public sector, and of more elderly workers. In line with very poor business sentiment, private sector employment is continuing to weaken.