Subscribers Only

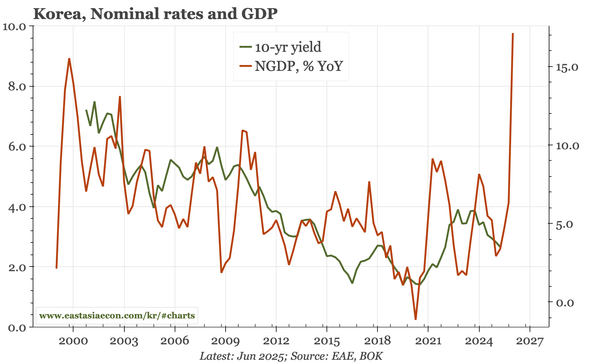

Korea – CA surplus of 20% of GDP still doesn't matter

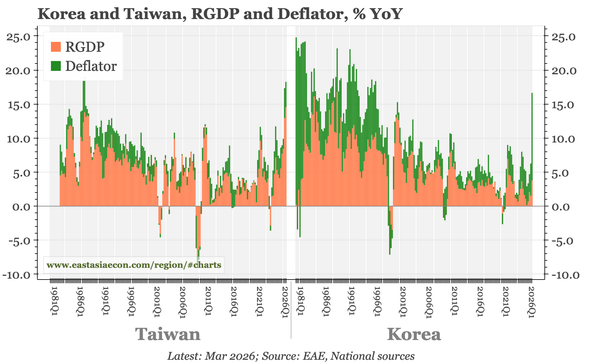

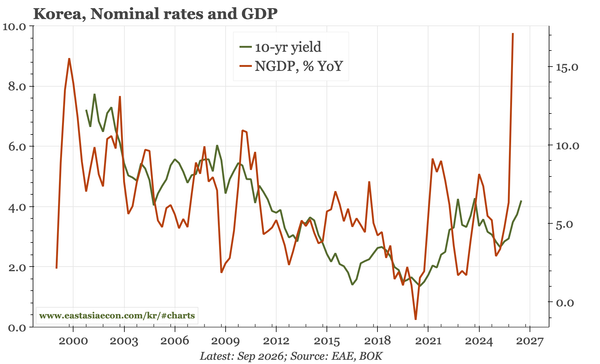

The flow story behind KRW weakness has transitioned from overseas buying by domestic retail to domestic selling by foreigners. Two other factors help inform the exchange rate: correlation with the JPY and, perhaps, a BOK that is late in hiking given the huge acceleration in NGDP growth.