Public Post

East Asia Today

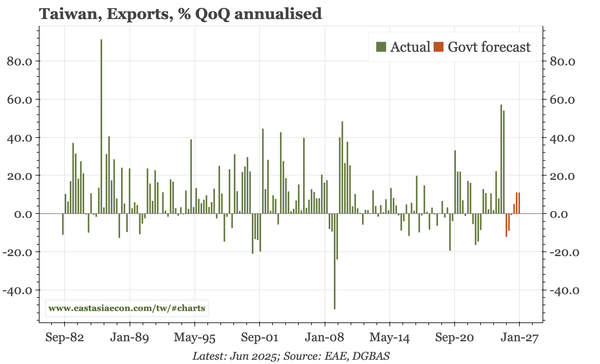

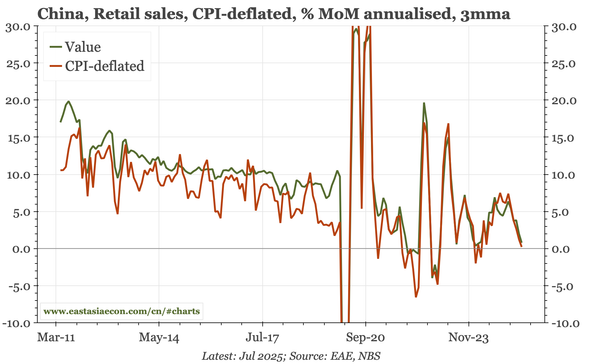

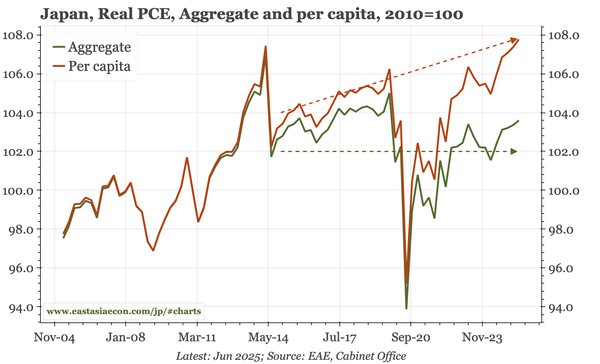

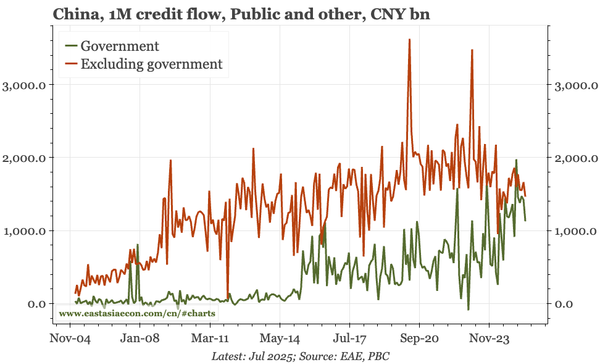

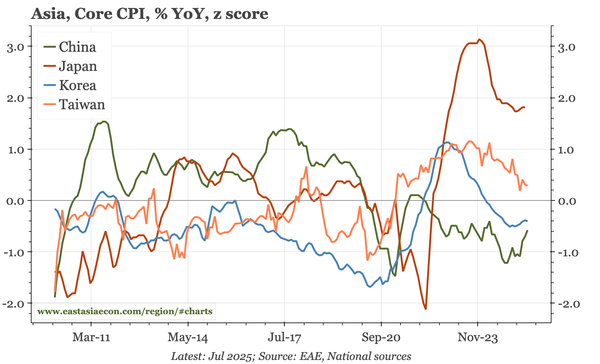

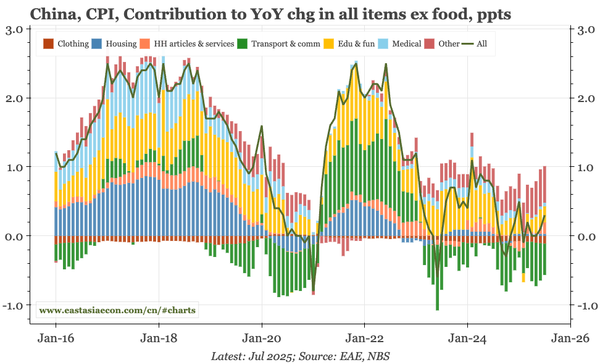

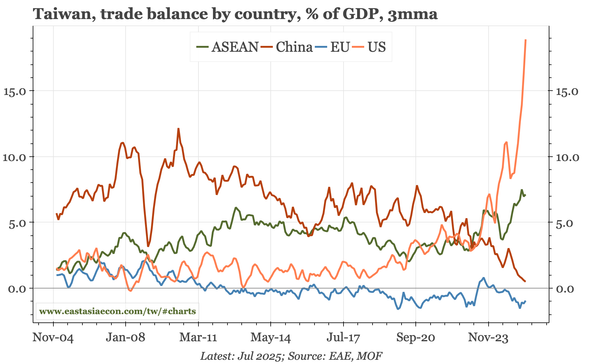

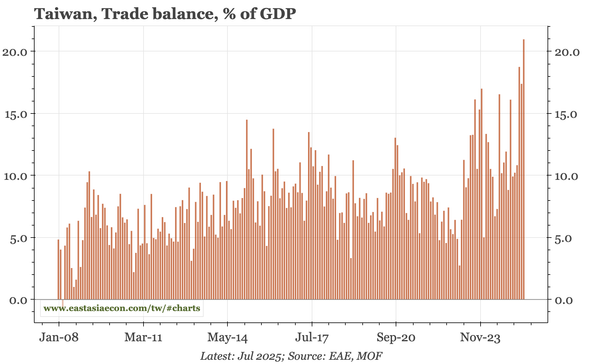

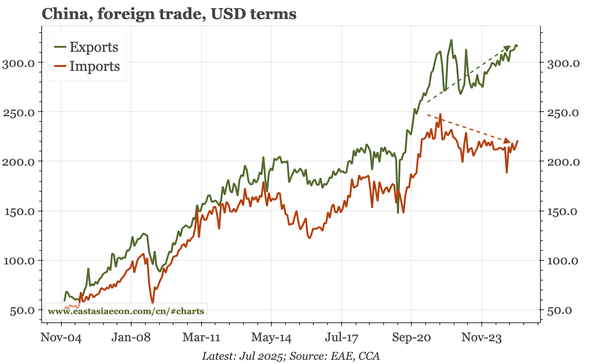

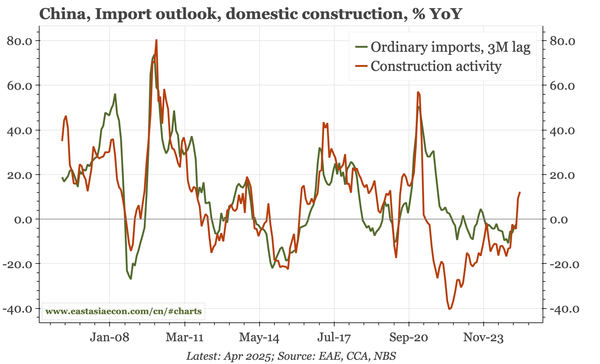

Many updates today. In China, property prices and the outlook for CPI, as well as the official activity data for July. The overall tone remains weak. By contrast, the first estimate of Q2 GDP data for Japan was solid. And detailed Q2 data for Taiwan, together with 2H25 forecasts, were more bullish.