Subscribers Only

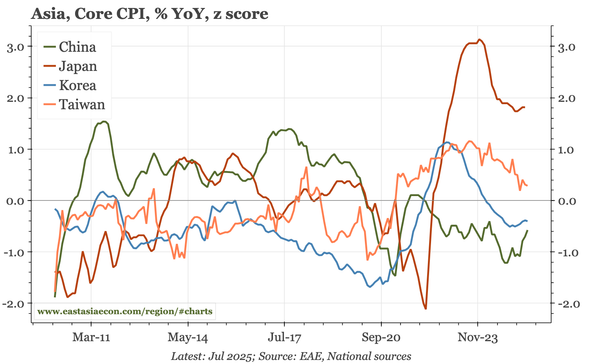

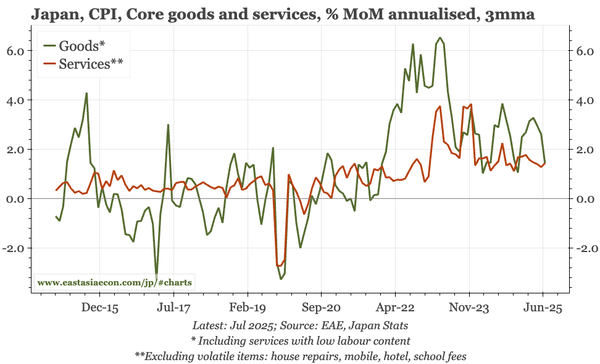

Japan – services PPI down again

The BOJ's inflation outlook is based on two dynamics: a waning of imported price inflation, but firmness in wages and inflation expectations. Services PPI is consistent with that framework. Headline is softening, but in sectors with high labour-intensity, it remains solid.