Subscribers Only

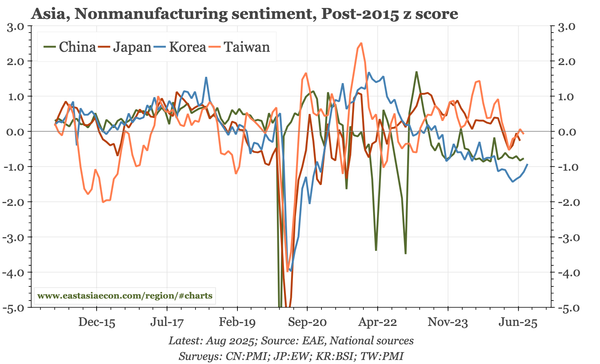

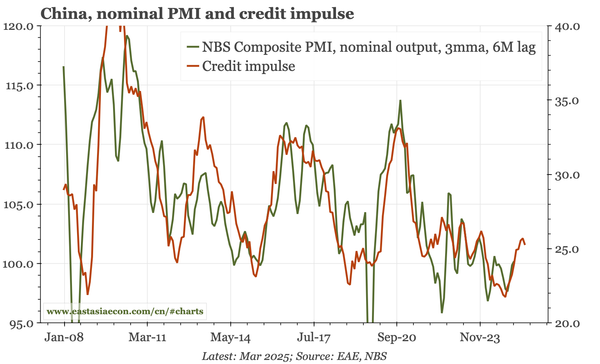

China – back to muddle through

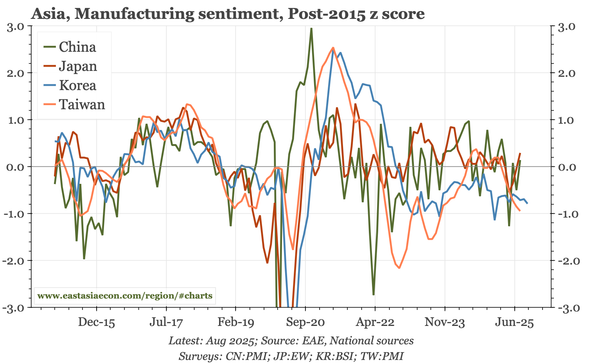

This discrepancy in the PMIs – S&P versions better, official PMIs still weak – is puzzling. Probably, the overall message is that China is back to a period of muddling through, with the cycle not robust, but getting some support from the better equity market and rise in the credit impulse.