Subscribers Only

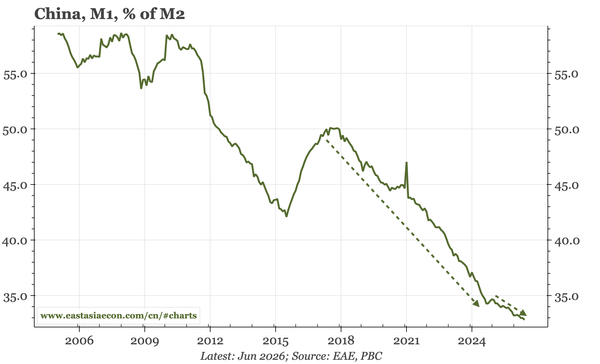

China – M1 growth slowing again

The continued slowdown in credit growth is led by households and CGBs – corporate borrowing has been firm. But the M1:M2 ratio is slipping again, warning that the domestic dynamic that had contributed to lessening deflation and a less dovish PBC is now once again fading.