Subscribers Only

East Asia Today

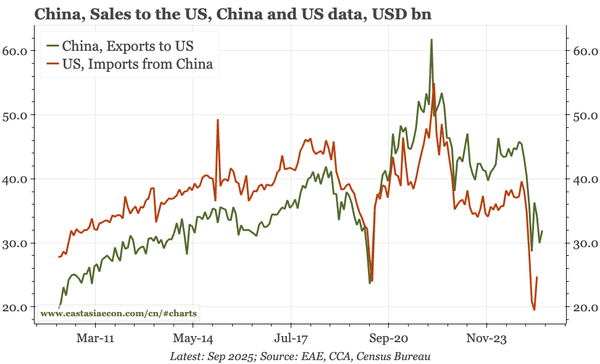

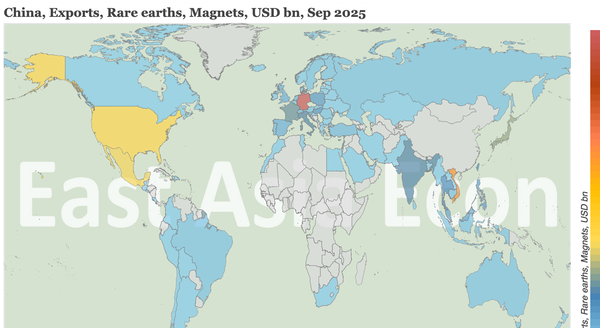

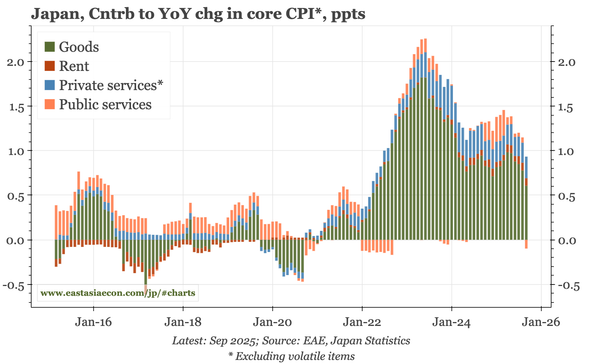

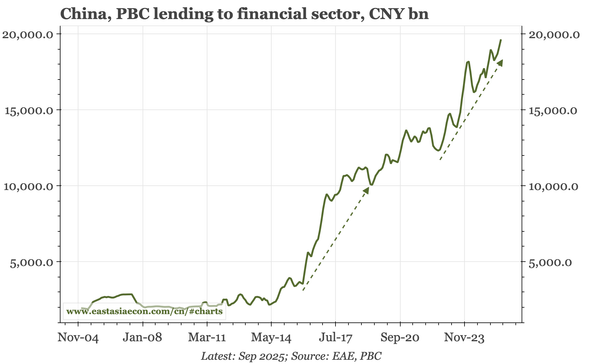

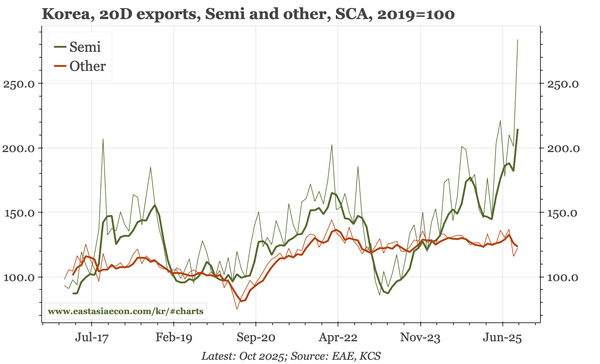

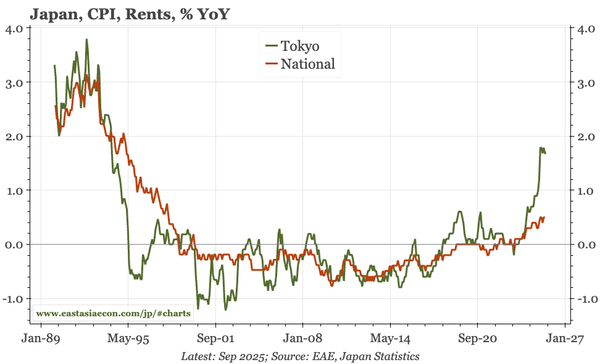

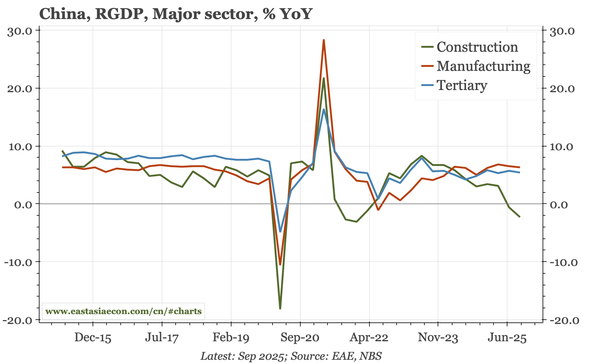

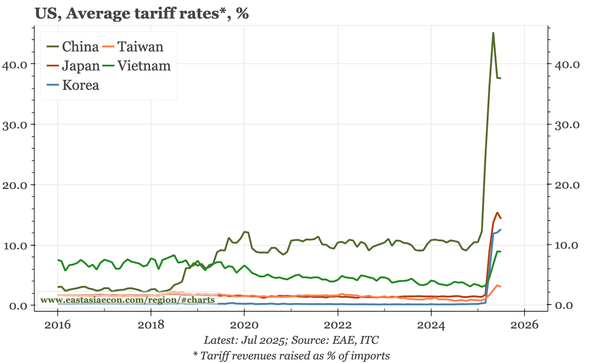

Lots of data today, with the usual month-end releases for China, Japan and Korea. Also interesting were the analytical boxes in the BOJ's outlook report. Finally, an update on tariffs after yesterday's China-US talks. The conclusion: with the CNY depreciating, China doesn't look very disadvantaged.