Subscribers Only

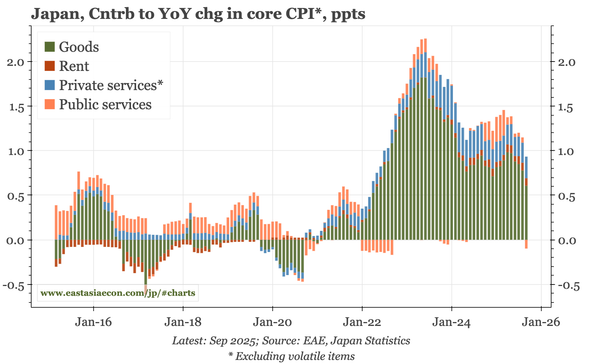

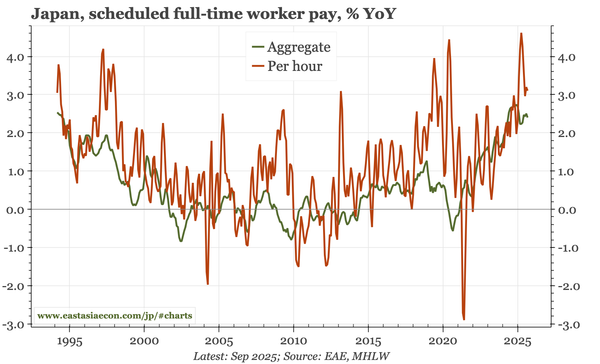

Japan – soft headline wages, details a bit better

Wage growth was softer in September. The continued slowdown in part-time wages per hour will be a bigger concern if it persists beyond the October rise in the minimum wage. Per hour full-time wage growth is stronger than the headline, though the data are noisy.