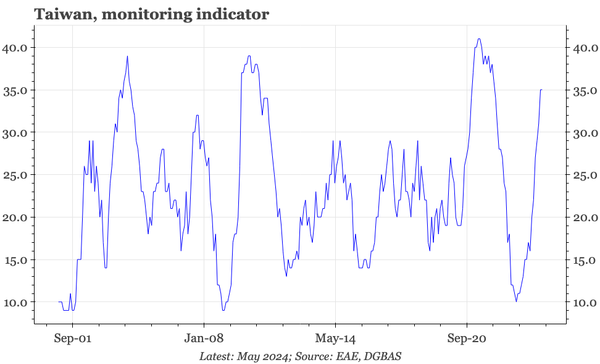

Public Post QTC: Taiwan – cycle momentum doesn't get better than this The official Monitoring Indicator that was updated today through May includes equity prices, but also real economy inputs like IP. It paints a picture of a pretty punchy recovery.

Public Post QTC: Japan – retail sales stronger Retail sales in May bucked the weakening of consumer confidence in recent months. That said, real retail sales remain lower than in September 2023. Consumption is still weak.

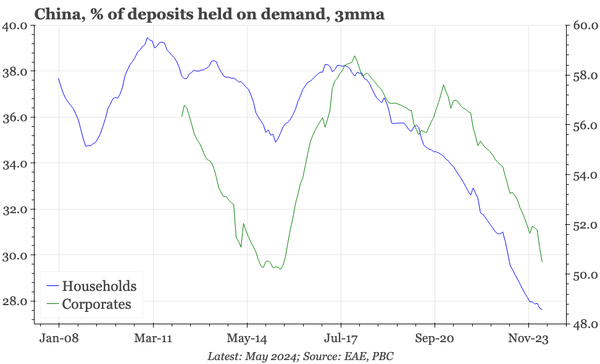

Public Post QTC: China – macro "lying flat" If you want to follow just one indicator in China, this is a good candidate. Li Yang has referred to it as "lying flat". If it doesn't change, it is very unlikely the trajectory of nominal growth will either.

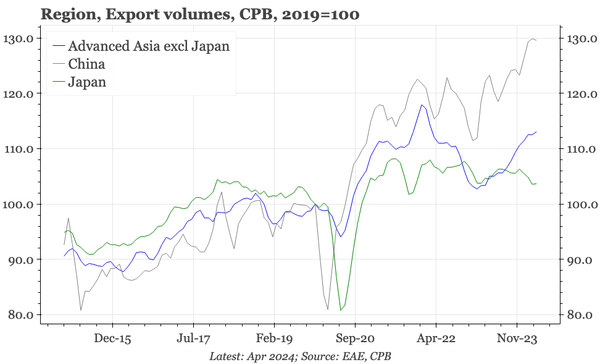

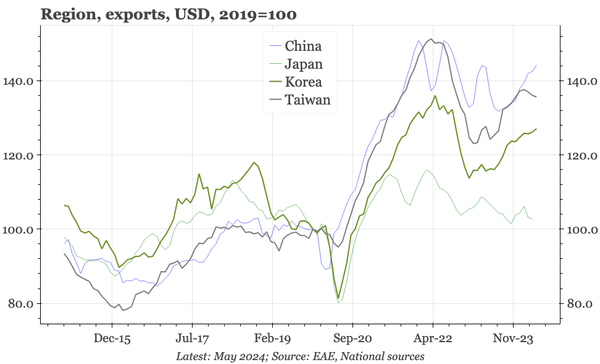

Public Post QTC: China – a new step-up in export volumes After flat-lining for much of 2022 and 2023, China's exports have now risen anew. After rising 20% during the pandemic, volumes have now increased a further 5%. That lift isn't being seen elsewhere in Asia.

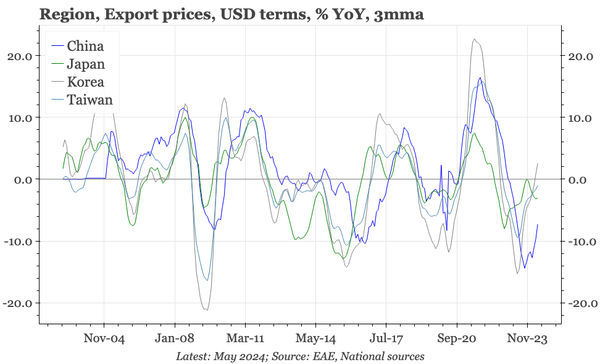

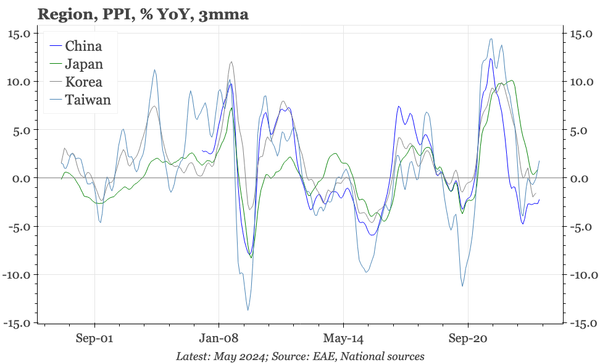

Public Post QTC: China – not an outlier in export prices With YoY export prices falling, China is exporting deflation. But most of the region has been too. The data continue to suggest export deflation from China is more cyclical than structural.

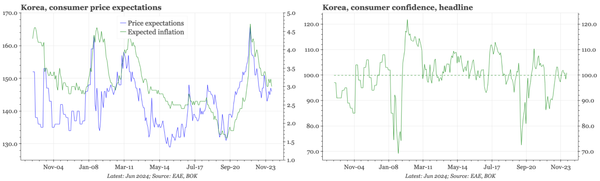

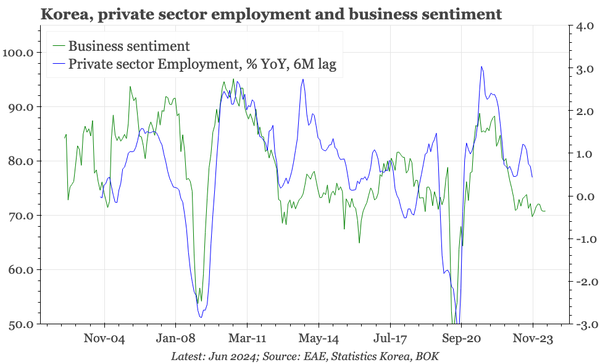

Public Post QTC: Korea – no change in consumer sentiment There's nothing in the June consumer confidence survey to shift the BOK. Confidence was neither strong nor weak. General price expectations ticked down, but picked up for property.

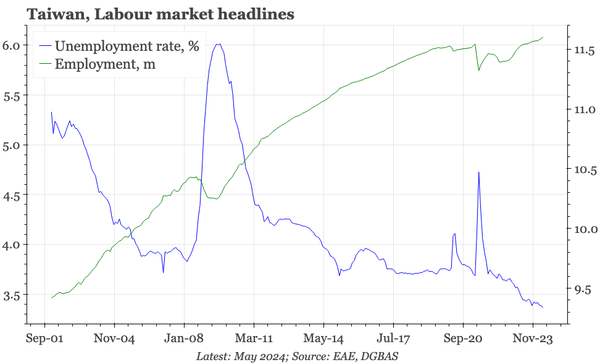

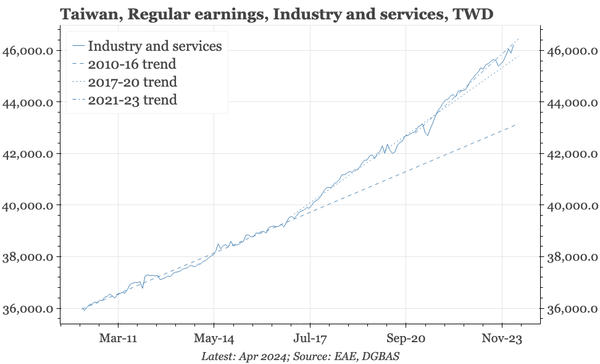

Public Post QTC: Taiwan – labour market still tightening Employment in May hitting a record high and unemployment edging down to a 23-year low aren't strong reasons to think the tightening cycle is over.

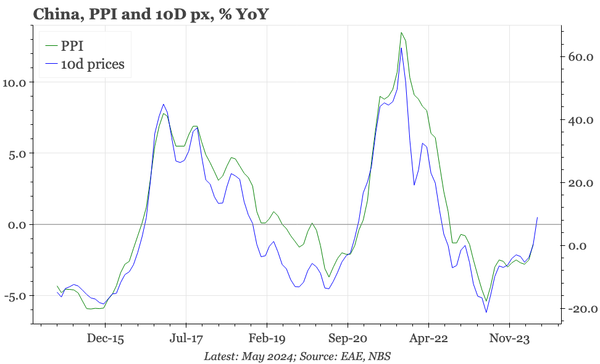

Public Post China – PPI firming further in June 10D prices show YoY PPI is on track to turn positive in June. That might, though, be it: MoM prices have ticked down so far this month, with the YoY rise all about the base effect.

Public Post QTC: China – liquidity preference down again Regulatory changes are causing big swings in deposit data, so caution is needed. But looking at M1 in relation to M2 should cancel some of the noise, so the fall in that ratio is concerning.

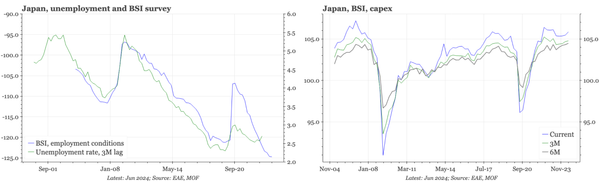

Public Post QTC: Japan – tight labour market, strong capex In today's Q2 BSI survey, overall sentiment didn't change much. But firms continued to report record levels of worker insufficiency, and capex intentions remained strong.

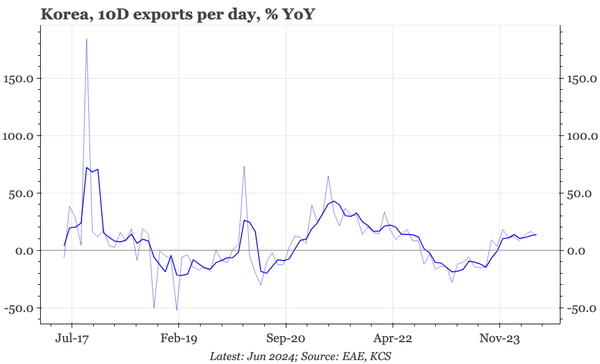

Public Post QTC: Korea – exports solid not spectacular The export data for the first 10 days tell the same story as other recent indicators: there is an export recovery, but it is modest, and doesn't look to be gaining further momentum.

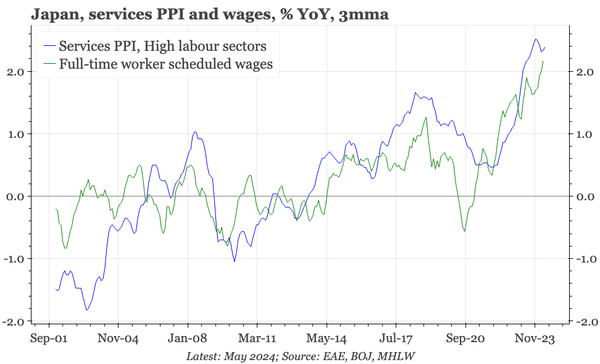

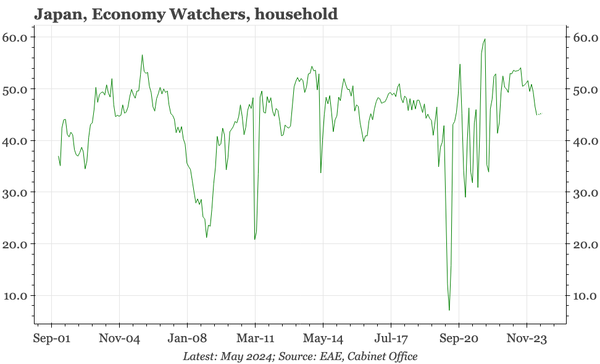

Public Post QTC: Japan – inflation bites The fall in the EW survey isn't surprising given higher inflation. But it shows the BOJ's dilemma: keep policy loose as aggregate demand is weak, or normalise to try to lift the JPY and real incomes.

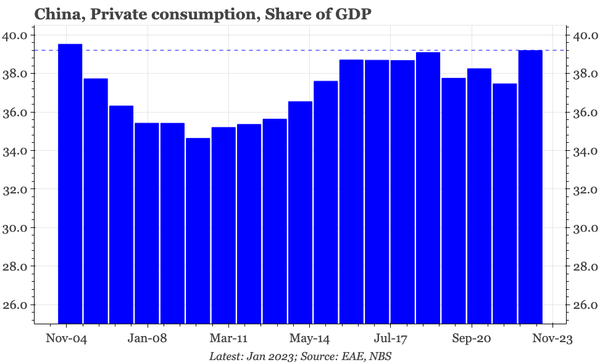

Public Post QTC: China – consumption share highest since 2005 Consumption isn't as weak as consumer confidence suggests: recently released full-year 2023 data show the consumption share surpassing – albeit only slightly – pre-covid levels.

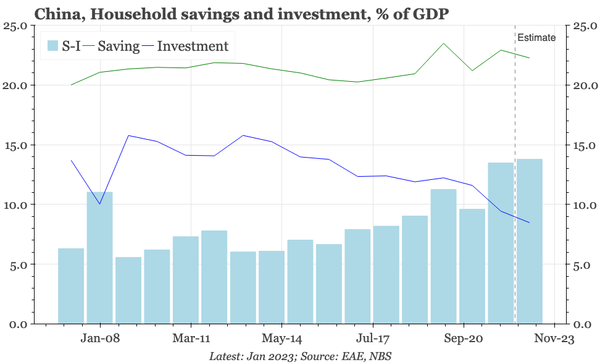

Public Post QTC: China – investment falls, savings don't Recently released FoF data for 2022 confirms no big change in household savings. But investment fell as spending on housing dropped. It should be no surprise the CA surplus has been widening.