Subscribers Only

East Asia Today

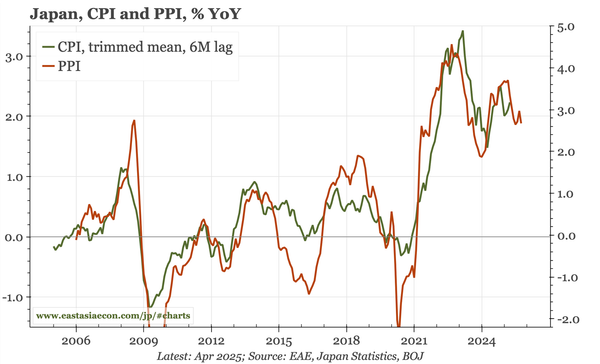

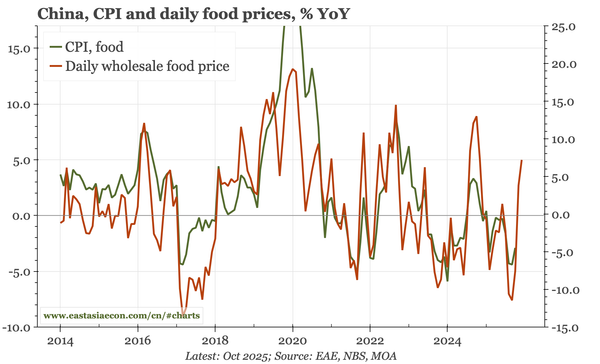

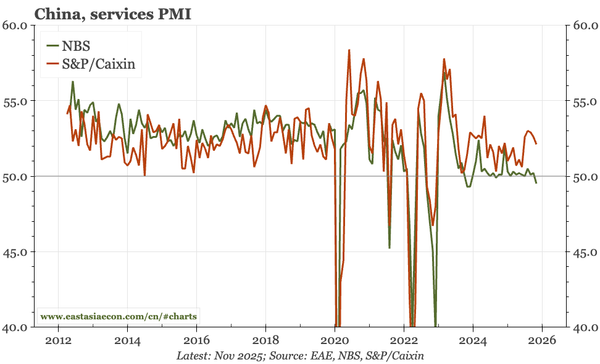

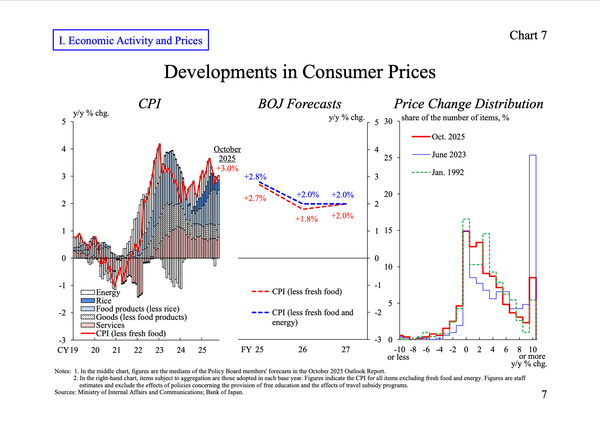

Goods PPI shows upstream inflation pressure in Japan remaining firm, while today's CPI and PPI releases in China point to a further lessening of deflation. Korea's labour market is complicated by supply-side changes. In Taiwan the message is simpler, with wage growth continuing to trend up.