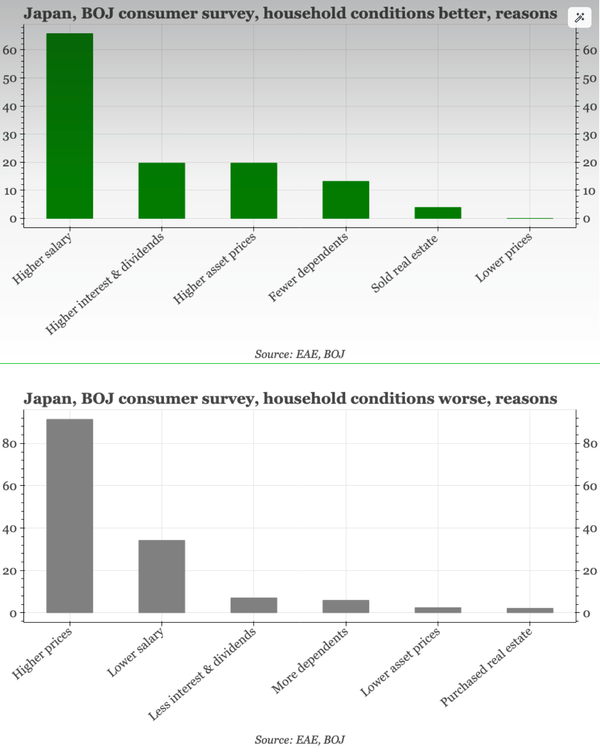

In the BOJ's Q2 survey, 65% of respondents saying they felt more positive cited higher incomes, an outcome helped by policy stimulus. But 90% of people saying they felt worse blamed higher prices, with low rates and the weak JPY also the result of policy.