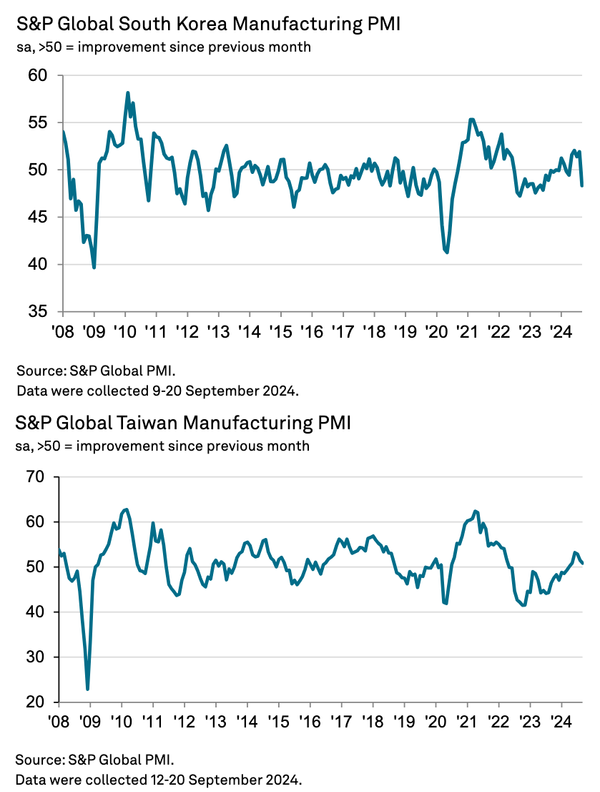

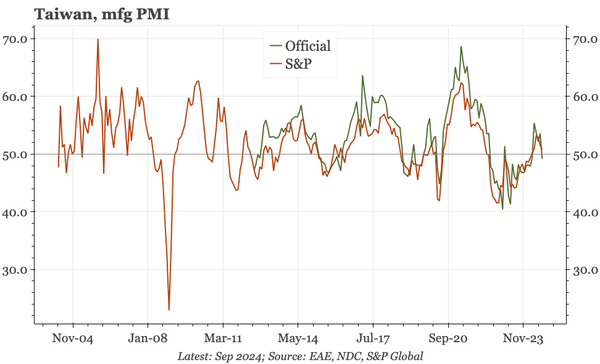

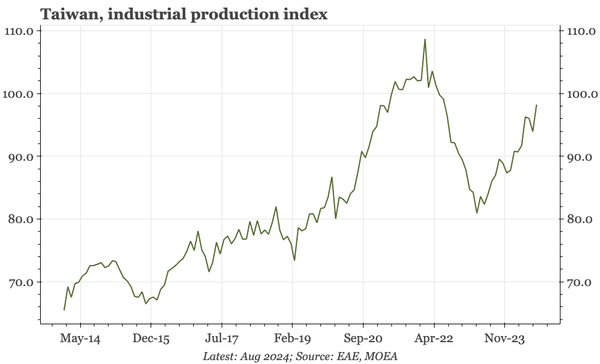

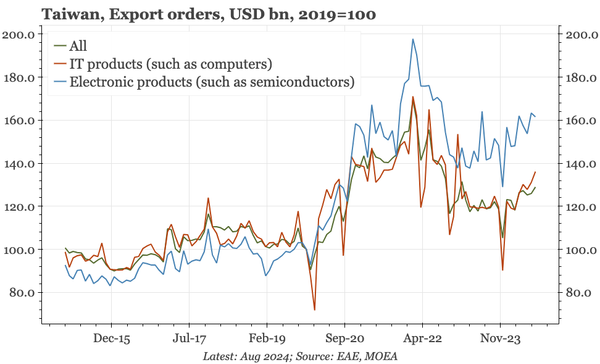

Taiwan manufacturing should be on a big upswing, driven by recovery from the 2022-23 recession, and AI demand for semis. And yet, even before now, data have been patchy, and the PMIs suggest that mfg started to contract again in September. If that's the end of the upturn, it didn't last long.