Subscribers Only

Last week, next week

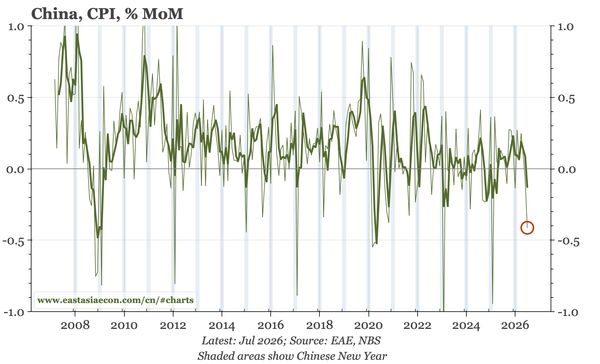

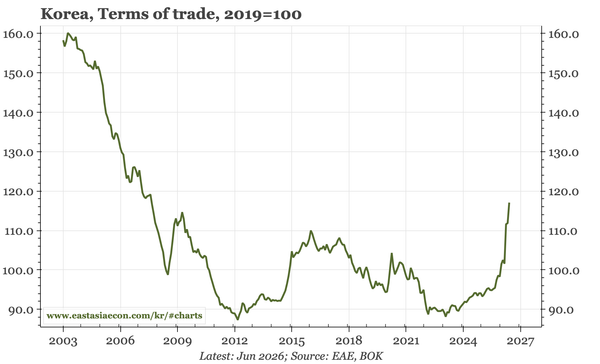

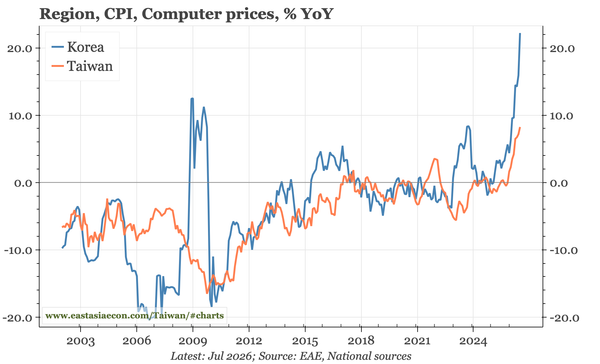

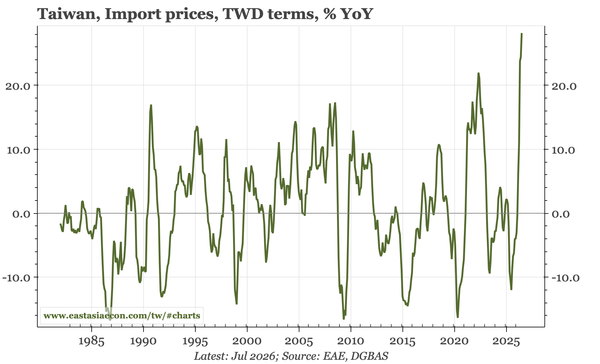

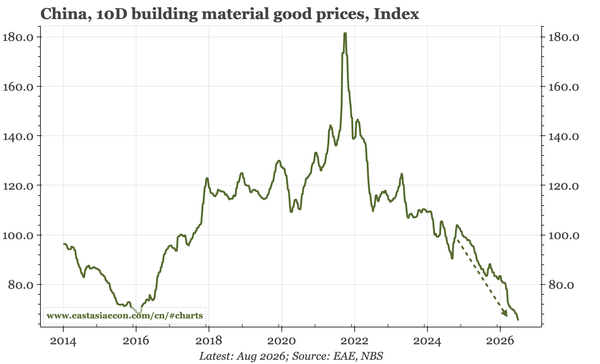

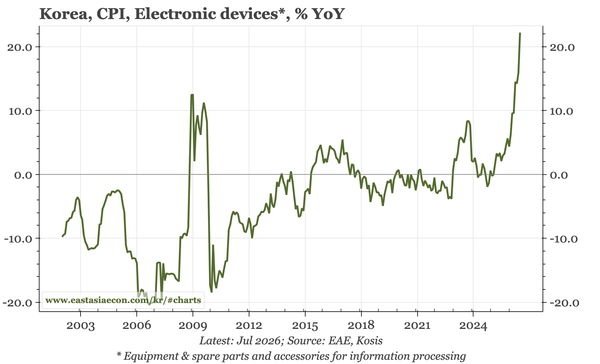

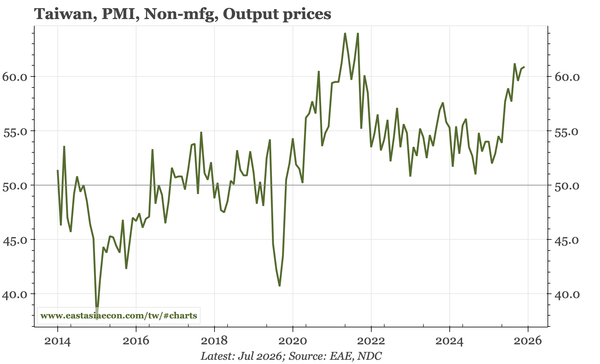

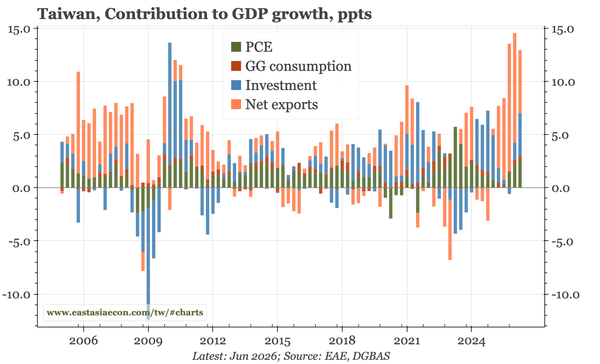

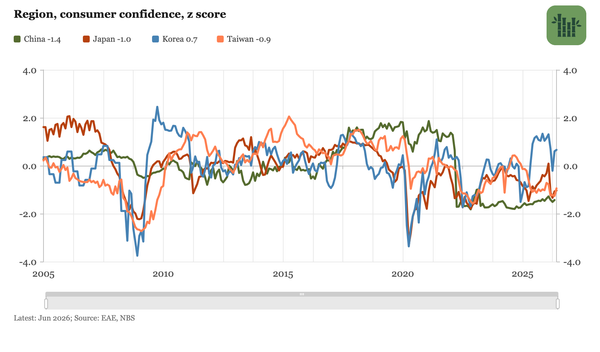

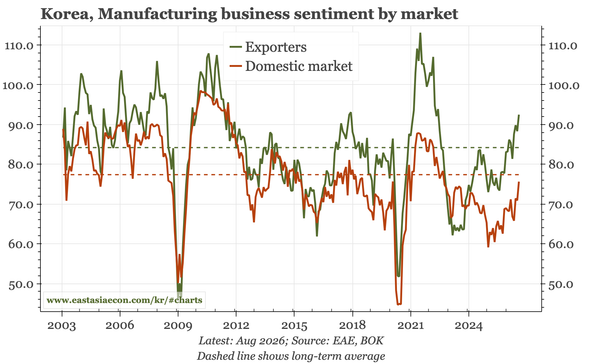

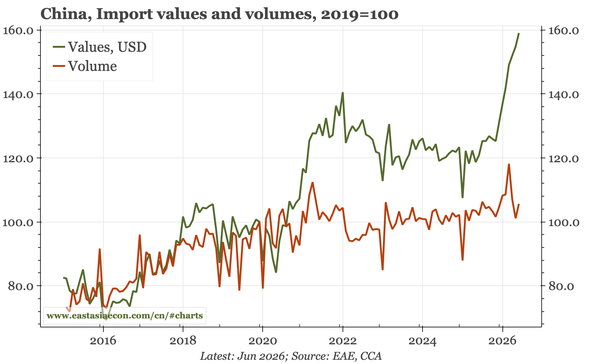

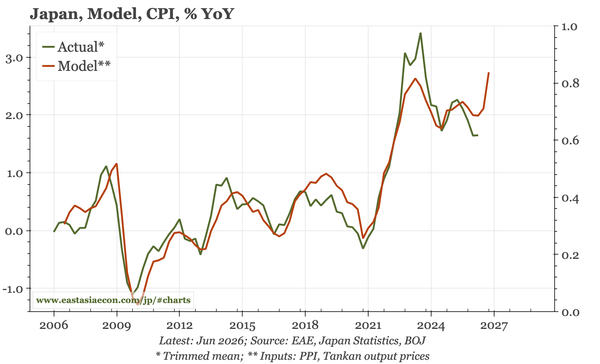

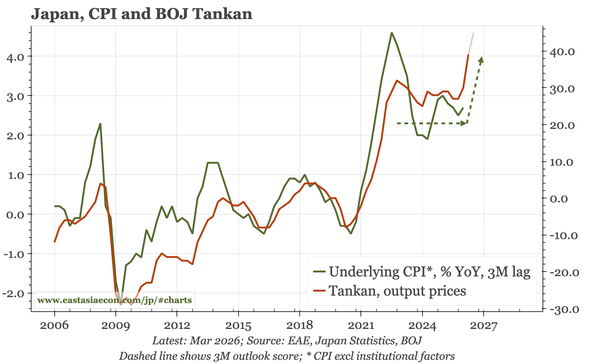

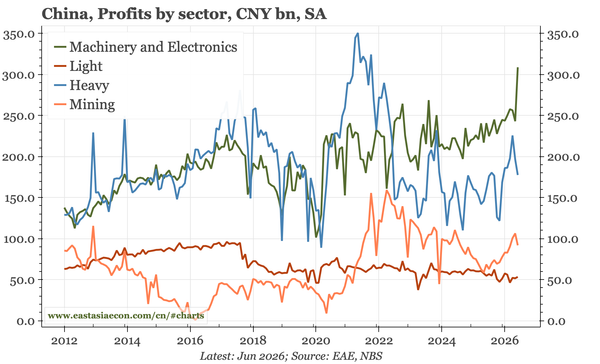

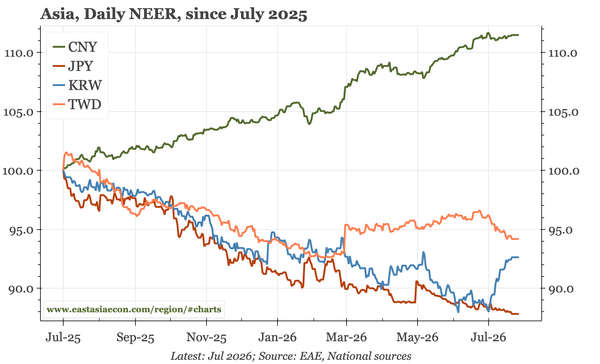

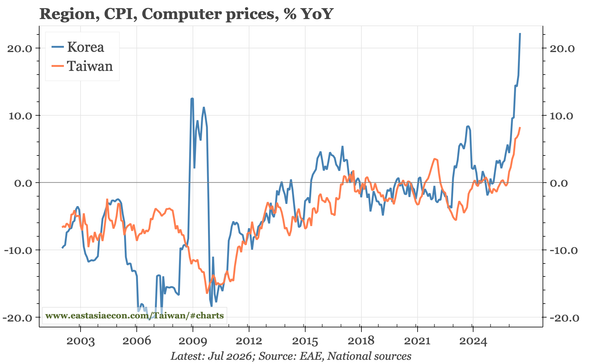

China macro is again a contrast between export strength and renewed deflationary pressure. Takaichi's sales tax cut doesn't look like the policy approach Bessent wants. For Korea, data an BOK analysis points to upside risks. In Taiwan, the key issue is lagged spillover from the 24-25 export boom.