Subscribers Only

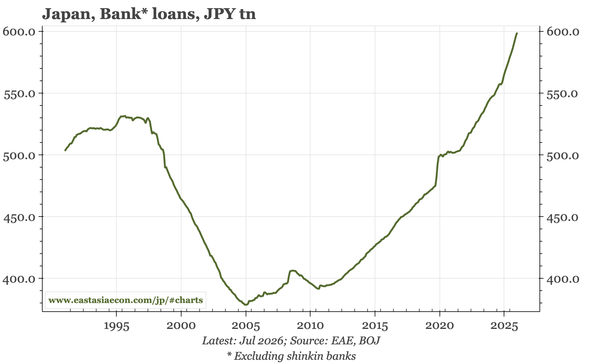

Japan – fiscal reality v rhetoric

A longer note on fiscal policy: the rhetoric of loosening versus reality of tightening of Abenomics and the early part of Takaichi's administration, the costs of that for the household sector versus the benefits for corporates, and what all that means for Takaichi's stance going forward.